When renting out bounce houses, liability risks are unavoidable. Injuries, property damage, and accidents caused by weather or equipment failure can lead to lawsuits. This is why additional insured endorsements are essential. These endorsements extend your insurance coverage to third parties like venues, schools, or event hosts, ensuring they’re protected if something goes wrong. Without this, many clients won’t sign contracts or allow equipment on their property.

Here’s what you need to know:

- What it is: An additional insured endorsement legally adds another party to your liability policy, covering their legal defense and settlements if sued due to your operations.

- Why it matters: Bounce house injuries send around 10,000 people to the ER annually. Venues often require this endorsement to safeguard themselves.

- Cost: Typically $50 per endorsement, or sometimes included in your policy at no extra charge.

- Process: Provide your insurer with the venue’s legal name and event details. Some venues also require specific forms or minimum coverage limits.

Skipping these endorsements could leave you exposed to lawsuits and cost you high-value clients like schools or parks. They’re a small price to pay for financial and legal protection.

What Additional Insured Endorsements Are

Certificate of Insurance vs Additional Insured Endorsement Comparison

Definition and Purpose

An additional insured endorsement is a legal addition to your liability insurance policy that extends coverage to third parties not originally named as policyholders.

For example, adding a venue, school, or municipality to your policy allows them to file claims directly if they face legal action due to your business operations. Let’s say a child is injured at a school carnival and the parents sue both you and the school district. If the school district is listed as an additional insured, your insurance will cover their legal defense, court fees, and any settlements.

The purpose of this endorsement is straightforward: it shields third parties from the financial burden of legal issues that might arise due to your activities. These endorsements generally cover areas like bodily injury, property damage, and advertising injury linked to your operations.

There are two types of additional insured endorsements:

- Blanket endorsements automatically cover all clients or subcontractors.

- Specific endorsements list each party by name.

Next, let’s break down how these endorsements differ from Certificates of Insurance.

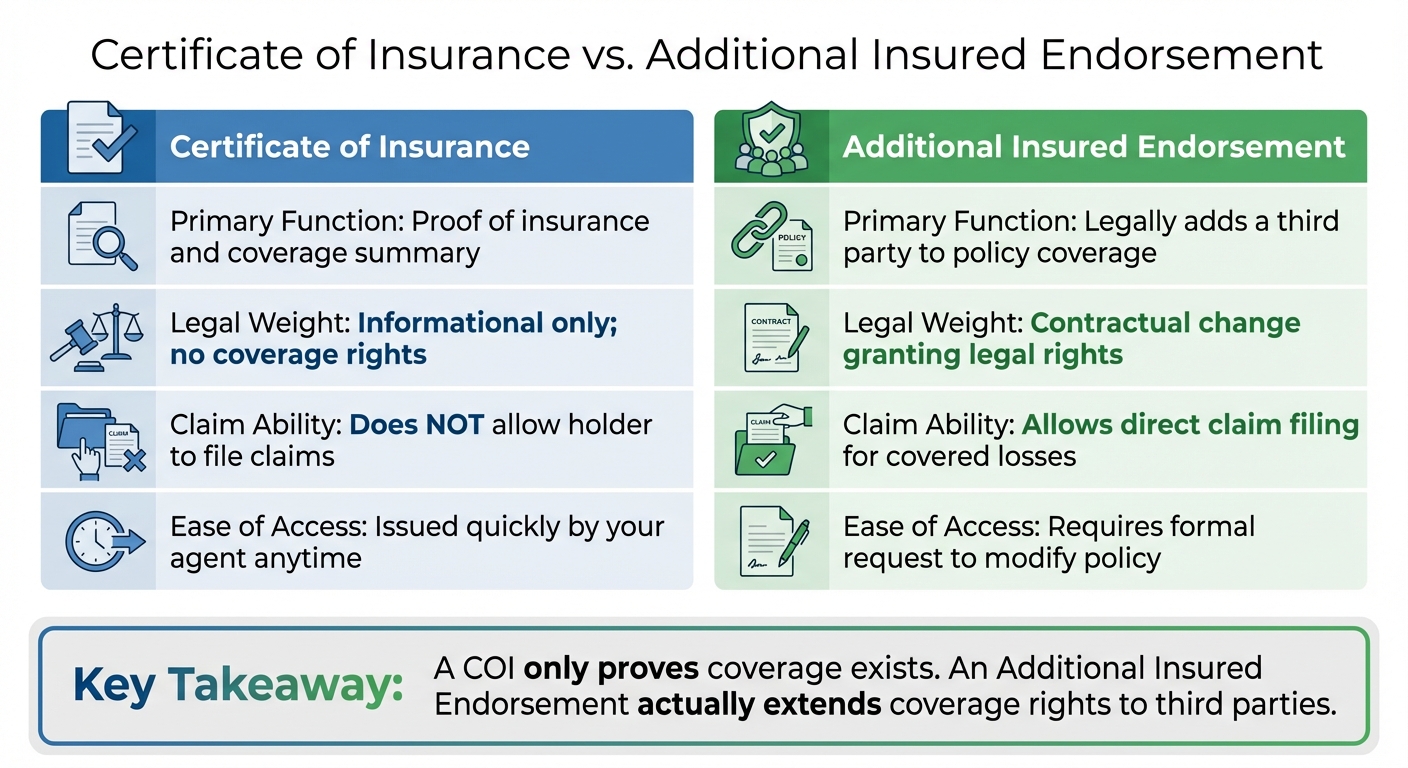

Additional Insured vs. Certificate of Insurance

It’s easy to confuse a Certificate of Insurance (COI) with an additional insured endorsement, but they serve very different purposes. A COI is simply a document that proves your policy exists and provides a summary of your coverage limits. On the other hand, an additional insured endorsement is a formal amendment to your policy that grants specific coverage rights to another party.

| Feature | Certificate of Insurance | Additional Insured Endorsement |

|---|---|---|

| Primary Function | Proof of insurance and coverage summary | Legally adds a third party to policy coverage |

| Legal Weight | Informational only; no coverage rights | Contractual change granting legal rights |

| Claim Ability | Does not allow holder to file claims | Allows direct claim filing for covered losses |

| Ease of Access | Issued quickly by your agent anytime | Requires formal request to modify policy |

"An additional insured endorsement… adds another insured party to the policy… extending coverage to an additional party." – Embroker Team

The distinction becomes critical when an incident occurs. If a venue only has a Certificate of Insurance, they would need to rely on their own insurance first and might later seek reimbursement from you. However, if they are named as an additional insured, your policy steps in directly to defend them, protecting their loss history and ensuring financial responsibility stays where it belongs.

Liability Risks in Bounce House Operations

Common Risks and Injury Claims

Renting out bounce houses comes with a host of liability risks. From the early 2000s to 2019, injuries linked to inflatables skyrocketed by 1,500%.

The most common injury claims stem from falls and collisions. When kids of varying sizes jump together, larger children can accidentally crash into smaller ones, leading to fractures, sprains, and other injuries. About two-thirds of these injuries involve arms and legs, while 15% affect the head or face. Equipment malfunctions, such as deflation or structural tears, can also cause the inflatable to collapse unexpectedly, posing serious risks.

Weather is another major factor, with high winds being particularly dangerous for inflatable stability. Operational mistakes – like setting up on uneven ground, failing to secure the unit with stakes or sandbags, or not providing proper adult supervision – further increase the chances of accidents.

Property damage is another concern. Bounce houses can harm lawns, fences, or other structures during setup or use. These risks highlight that liability goes beyond just equipment issues and extends to how the operation is managed overall.

Who Gets Held Liable

With so many risks involved, determining who is responsible becomes essential. Rental companies usually hold primary liability for injuries caused by improper setup, faulty equipment, or negligence by their staff. However, event hosts and homeowners can also share liability, especially if injuries occur due to inadequate supervision while the bounce house is under their care. Although liability waivers are often used to shift some responsibility, they don’t eliminate all risks.

Property owners and venues – like parks, schools, or corporate spaces – are often included in lawsuits simply because the accident happened on their premises. To protect themselves, these entities typically require being added as an additional insured on the renter’s insurance policy before allowing equipment on-site.

"If a foreign company does not have a U.S. liability insurance then the entity who imports a product from that foreign company is considered to be the manufacturer or producer and takes full responsibility of liability." – Bouncer Depot

Businesses importing equipment from uninsured foreign manufacturers can face full product liability. Additionally, employees involved in the physically demanding setup process can create another layer of liability if they get injured on the job.

These factors emphasize the importance of naming venues and event hosts as additional insured parties to mitigate potential financial risks.

When You Need Additional Insured Endorsements

Venue and Event Requirements

Before setting up a bounce house, venues often require proof of insurance. Public parks, schools, corporate facilities, and religious organizations typically demand an additional insured endorsement before issuing permits or signing contracts.

Take the City of Seattle, for example. They require all Special Event Permits to include proof of insurance coverage for the duration of the permit, stating:

"The City of Seattle requires that all Special Event Permits be supported by evidence of insurance coverage for the term of the permit".

Similarly, UC Berkeley mandates that student organizations and vendors name both the Registered Student Organization (RSO) and The Regents of the University of California as additional insureds before permitting inflatables on campus. The Roman Catholic Archdiocese of Boston offers a comparable guideline, advising parishes to:

"always request a Certificate of Insurance from the vendor. The certificate should name your parish/school, the Roman Catholic Archdiocese of Boston and Bishop Richard Henning, a Corporate Sole as additional insured for the scheduled event".

Corporate venues and private recreational facilities also have similar requirements to protect themselves from liability claims. These examples highlight the importance of customizing your insurance to meet the specific demands of each event.

Coverage Limits and Submission Deadlines

Understanding coverage limits and submission deadlines is just as important as meeting venue requirements. Coverage amounts can vary significantly. For instance, the City of Seattle requires $2 million in liability coverage for inflatables, while Lehi City and UC Berkeley set the minimum at $1 million. Some municipalities, like Lehi City, also require additional coverage details, such as $3 million in aggregate coverage and a $500,000 sub-limit for damages to rented premises.

Timeliness is crucial, too. For example, the City of Seattle mandates submitting insurance documentation at least 30 days in advance for risk management review. When requesting an endorsement, it’s essential to include the venue’s full legal name and event address during booking. Additionally, using specific ISO forms like CG 20 12 or CG 20 26 and listing the coverage as "primary and non-contributory" to the venue’s insurance can help avoid rejection due to generic wording.

How Additional Insured Endorsements Protect Your Business

Reducing Liability Exposure

Additional insured endorsements act as a financial safeguard for your bounce house rental business, shielding you from potential lawsuits. When a venue or client is added as an additional insured on your policy, your insurance provider steps in to handle their legal defense if they’re sued due to an accident involving your equipment. This means your policy directly covers those legal expenses.

These endorsements also help maintain your business’s loss history by ensuring that claims are assigned to the correct party’s insurance. This can prevent your premiums from rising unnecessarily. As the Embroker Team puts it:

"The main benefit of an additional insured endorsement is that it will reduce the impact of the policy owner’s loss history since the additional insured status serves to make sure that the financial responsibility of the claim is placed on the policy of the party that is most likely to be responsible for the claim".

Another key advantage is protection against vicarious liability. This comes into play when venues could be held accountable simply because they allowed your inflatable equipment on their property. By including an additional insured endorsement, venues are protected from being unfairly blamed for incidents they didn’t directly cause.

Without these endorsements, you risk losing access to high-value clients like schools and parks, which often require direct access to your policy limits. This could hinder your ability to tap into these profitable opportunities. Beyond legal protection, these endorsements also simplify your administrative tasks, making it easier to manage client relationships and compliance.

Cost and Administrative Process

After addressing liability concerns, managing the process of securing these endorsements is straightforward. On average, endorsements cost about $50 each. However, many insurance providers include unlimited endorsements as part of your annual policy, free of charge. Considering that bounce house liability insurance typically costs between $1,800 and $2,500 annually, the price of individual endorsements is a small investment for the protection they offer.

To obtain an endorsement, you’ll need to provide your insurance broker with the venue’s legal name and event address. They will then generate the necessary documentation using the appropriate ISO form, such as CG 20 12 or CG 20 26. Be sure to request a copy of the actual endorsement document, not just the certificate, as insurers don’t automatically send proof to third parties.

For added convenience, blanket endorsements can cover multiple clients automatically, saving you time and effort on administrative tasks.

Required Documentation and Compliance

Preparing Certificates of Insurance

When preparing your Certificate of Insurance (COI), it’s crucial to use the venue’s exact legal name. For example, the University of Missouri requires the name "The Curators of the University of Missouri", while UC Berkeley specifies "The Regents of the University of California". Using an incorrect name can slow down the approval process or even disqualify your booking.

Most venues require $1 million in commercial general liability coverage, though some municipalities may ask for up to $3 million in aggregate limits. If your event involves driving equipment onto the property or bringing in staff for setup, you’ll also need $1 million in automobile liability coverage and proof of statutory workers’ compensation. Additionally, venues often request your rental contract, participant waivers, and official safety guidelines for their risk management team to review.

To avoid delays, submit all required documentation at least 10 business days in advance. Some areas, like Los Angeles, use digital systems such as KwikComply.org to verify vendor insurance online. Keep in mind that processing additional insured endorsements through your insurance company may take longer than a standard COI, so it’s wise to request these endorsements as soon as you secure the venue. Once submitted, ensure that you consistently maintain updated records.

Keeping Records Current

Staying compliant doesn’t stop after the initial submission – keeping your records up-to-date is just as important. For instance, in Texas, operators of inflatable devices must obtain an annual Texas Amusement Ride Compliance Sticker for each unit. Each sticker costs $40 and requires proof of current insurance. The Texas Department of Insurance updates its compliance list weekly, so any lapse in coverage could immediately disqualify you from bookings.

To stay on top of requirements, conduct an annual insurance review and use a calendar to track policy, permit, and sticker renewal dates. It’s also a good idea to maintain detailed equipment maintenance logs and safety training records. Venues may request these documents to verify compliance, and providing them can sometimes lower your insurance premiums. Accurate and organized documentation not only ensures compliance but also reinforces the protection offered by additional insured endorsements.

Conclusion

When running a bounce house rental business, managing liability risks is non-negotiable, and additional insured endorsements play a key role in safeguarding your operations. Given the potential for accidents, having the right coverage ensures that legal defense fees, court costs, and settlements are handled by your insurance when incidents arise.

These endorsements go beyond protecting third parties like venues, schools, and event hosts – they also shield your financial stability. As noted by the Embroker Team, they help shift financial responsibility to the party at fault, reducing the impact on your loss history. This can lessen claims on your primary policy and may even lead to lower insurance premiums over time.

For many high-value clients, such as schools, municipalities, and corporate venues, additional insured status is often a requirement. At approximately $50 per endorsement – or sometimes included as part of a flat-rate option – this modest expense provides important legal and financial protection. It also strengthens your risk management approach while meeting client expectations.

Keeping your documentation current is another essential layer of protection. Ensuring endorsements cover both ongoing and completed operations, maintaining accurate safety records, and staying compliant not only builds trust with clients but also supports the long-term success of your business. These practices reflect a commitment to responsible and professional operations.

FAQs

Why do venues ask for additional insured endorsements when renting bounce houses?

Venues frequently ask bounce house rental companies to include them as an additional insured on their liability insurance policy. This provision ensures the venue is covered under the policy for any injuries or property damage that might happen during the event.

With this endorsement in place, the venue is shielded from financial liability in case of accidents. It provides them with reassurance while simplifying the process for you to host your event without added hurdles. It’s an important measure for managing risks and ensuring all parties have the protection they need.

Why are additional insured endorsements important for bounce house rentals?

An additional insured endorsement broadens the rental company’s liability coverage to include the venue where the bounce house is being used. In practical terms, this means that if something goes wrong – like someone getting hurt or property being damaged – both the rental company and the venue are protected under the same insurance policy.

This extra layer of coverage takes care of legal expenses, court costs, and even potential settlements, relieving both parties of significant financial stress. For businesses like Bouncy Rentals USA, this type of insurance isn’t just a nice-to-have – it’s a must. It helps reduce risks and builds trust with both venues and customers.

How do I get an additional insured endorsement for my bounce house rental event?

Obtaining an additional insured endorsement for your bounce house rental event is simpler than you might think, and it’s a smart way to protect both yourself and the event venue from potential liability. Here’s how it usually works:

- Identify who needs to be added: This is typically the park, school, or venue hosting your event.

- Reach out to your insurance provider: Request an additional insured endorsement for the event. Be ready to provide details like the event date, location, and the name of the entity to be added.

- Double-check the endorsement: Make sure it aligns with the venue’s requirements, including liability limits (commonly $1,000,000).

- Get a Certificate of Insurance (COI): Once the endorsement is in place, obtain the COI and share it with the venue. It’s best to do this at least two weeks before the event.

Taking these steps ensures that the venue is covered under your policy, allowing businesses like Bouncy Rentals to focus on creating memorable party experiences without unnecessary risks.