Inflatable rental insurance is a must-have for protecting your business from financial risks like injuries, property damage, or lawsuits. Here’s what you need to know:

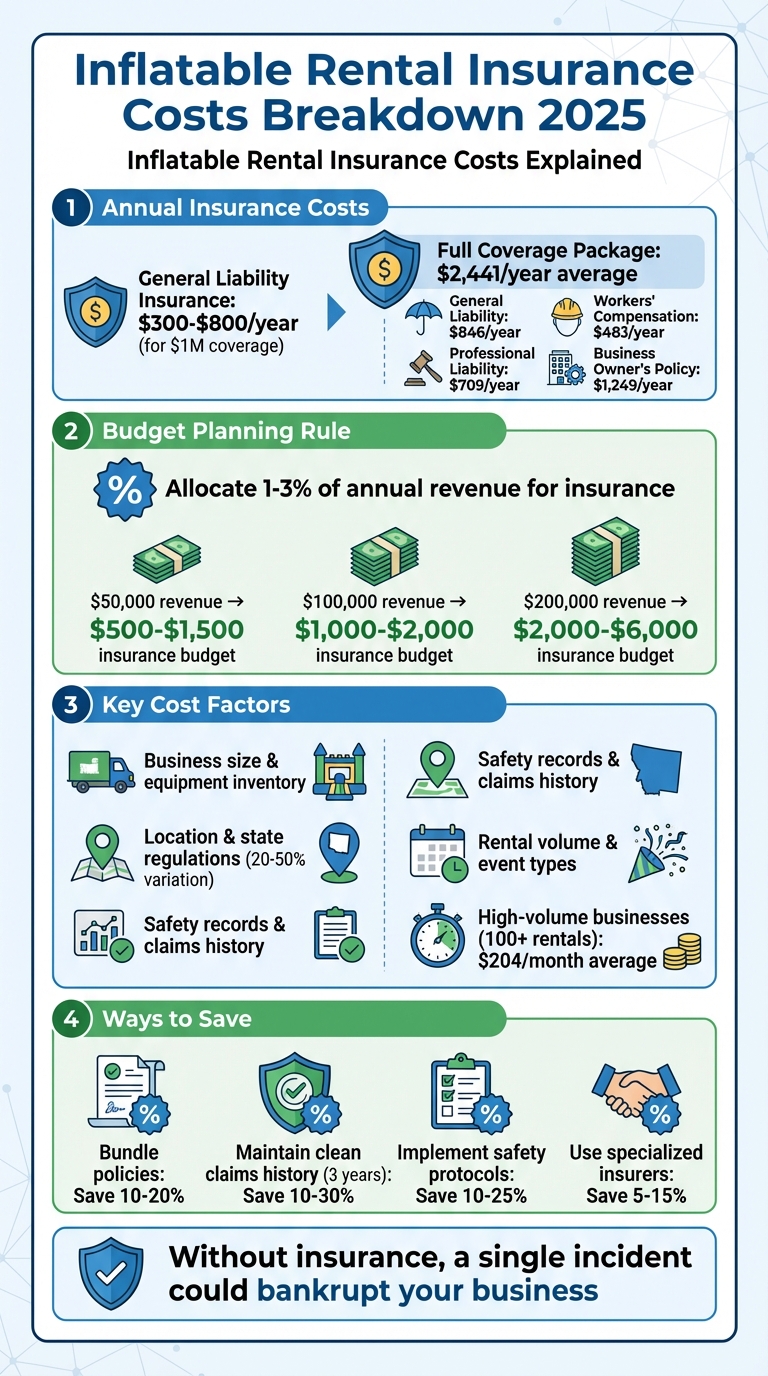

- General liability insurance: Costs between $300 and $800 annually for $1 million in coverage. This is the most important policy for covering guest injuries and property damage.

- Full coverage packages: Average around $2,441 per year, including general liability, workers’ compensation, and inland marine insurance.

- Factors affecting costs: Business size, location, equipment inventory, safety record, and rental volume.

- Ways to save: Bundle policies, maintain a clean claims history, implement safety protocols, and get quotes from specialized insurers.

Without insurance, a single incident could lead to overwhelming costs, from medical bills to legal fees. Planning your budget with 1–3% of annual revenue for insurance can help you avoid surprises. Prioritize safety and shop around for tailored coverage to protect your business and ensure long-term success.

Inflatable Rental Insurance Costs Breakdown 2025

Types of Insurance Coverage for Inflatable Rentals

Running an inflatable rental business involves juggling various risks, which is why most operators rely on a mix of insurance policies like general liability, product liability, inland marine, workers’ compensation, and umbrella policies. These policies not only address specific risks but also play a big role in determining your overall insurance costs.

General Liability Insurance

General liability insurance is the backbone of your coverage and often the most expensive part of your policy package. It protects against guest injuries, property damage, and legal defense costs.

Many venues – like schools, churches, parks, and city facilities – require proof of general liability coverage before allowing you to operate. Typically, they mandate at least $1 million per occurrence and $2 million aggregate. For U.S.-based businesses, basic general liability coverage usually costs between $300 and $800 annually for $1 million in protection. However, the actual premium depends on factors like your location, the size of your equipment inventory, and whether you’ve had prior claims. Considering the high risk of slip-and-fall incidents during children’s activities or outdoor setups, this coverage is a must-have for any inflatable rental business.

Product Liability Insurance

Product liability insurance steps in when an inflatable or its components are found to be defectively designed, manufactured, or labeled, leading to injury or property damage. For instance, if an inflatable malfunctions due to a manufacturing defect, this policy would cover the resulting claims.

This type of insurance is different from general liability, which typically covers issues related to how the equipment is set up or used – like improper anchoring or inadequate crowd management. Product liability is often bundled with general liability or added as an endorsement, making it essential for businesses that use inflatables from various manufacturers or purchase secondhand equipment.

Inland Marine Insurance

Inland marine insurance, also known as property-in-transit coverage, protects your equipment from risks like theft, fire, vandalism, vehicle accidents, and weather damage. This coverage applies whether your inflatables are in storage, being transported, or set up at an event.

For example, if a trailer full of inflatables is stolen or an accident damages your equipment while en route to a school carnival, inland marine insurance can cover repair or replacement costs up to the policy’s limits. Premiums depend on the value of your equipment and your chosen deductible. Opting for higher deductibles and accurately scheduling replacement values can help keep costs manageable. This coverage is particularly important for businesses with substantial inventory, such as companies managing tens of thousands of dollars’ worth of inflatables.

Workers’ Compensation Insurance

Workers’ compensation insurance covers medical bills, lost wages, and rehabilitation costs for employees injured on the job, regardless of who’s at fault. It also shields your business from most employee injury lawsuits. Common risks include lifting injuries and other hazards related to outdoor work.

In most U.S. states, workers’ compensation is mandatory as soon as you hire your first employee. Premiums are influenced by factors like payroll size, job roles, and your company’s injury history. For small inflatable rental businesses, workers’ compensation typically costs about $40 per month, or roughly $483 annually, when included in a broader insurance package.

Umbrella Insurance Policies

An umbrella policy, also known as excess liability insurance, provides additional coverage beyond the limits of your primary policies. This type of insurance is especially useful for large events or businesses with high-risk equipment, as it covers catastrophic claims that exceed the limits of your general liability policy.

For instance, if you have a $1 million general liability limit, you might add an umbrella policy ranging from $1 million to $5 million to handle severe incidents. While umbrella policies increase your overall premiums, they are often more affordable per additional million dollars of coverage than raising the limits on individual policies. This makes them a cost-effective way to meet venue requirements and protect a growing business.

Together, these insurance policies form the foundation of your risk management strategy and directly influence your overall premium costs, as outlined in the next section.

What Affects Insurance Costs

When it comes to insurance premiums, several factors come into play, each reflecting your business’s unique risk profile. By understanding these variables, you can better anticipate costs and even identify ways to manage or lower them.

Business Size and Equipment Inventory

The size of your business and the equipment you own are key factors in determining your premiums. Smaller operations with just a couple of bounce houses generally fall on the lower end of the cost spectrum. However, businesses with larger inventories – think obstacle courses, water slides, or interactive games – can see their premiums climb to $1,500 or more. The total value of your equipment also plays a role since insurers need to account for the cost of replacing items under inland marine coverage.

Location and State Regulations

Where you operate has a significant impact on your insurance costs. Rates can vary widely by state due to differences in local laws, compliance requirements, and regional risk factors like weather or population density. On average, general liability coverage costs around $70 per month (or $846 annually), but premiums can fluctuate by 20-50% depending on location. For instance, businesses in high-litigation states like California or densely populated urban areas usually face higher rates compared to those in rural regions with fewer regulatory hurdles.

Safety Records and Claims History

A strong safety record can work in your favor when it comes to insurance costs. Companies that consistently document safety procedures, maintain their equipment, and train staff are seen as lower-risk by insurers. Maintaining a clean claims history over three years can lead to a 10-30% reduction in premiums. On the flip side, even a single injury claim can significantly increase your rates. Regular inspections, detailed maintenance logs, and robust safety protocols demonstrate to insurers that you’re serious about minimizing risks.

Rental Volume and Event Types

How often you rent out equipment and the types of events you cater to also influence your premiums. High-volume businesses handling over 100 rentals annually are considered higher risk, with insurance bundles averaging around $204 per month. The nature of your events is another factor – large festivals, corporate gatherings, or crowded public events carry more liability than small backyard parties. Seasonal businesses that operate less frequently and focus on smaller, low-risk events may keep their monthly costs under $100 by limiting exposure to large-scale or complex operations. Knowing these cost drivers can help you plan your insurance budget more effectively.

Insurance Costs and Budget Planning

Average Annual Costs

As of 2025, the annual cost of general liability insurance for small inflatable rental businesses ranges between $300 and $800 for $1 million in coverage. For larger operations or those requiring broader protection, premiums can climb higher.

If you opt for a full coverage package that bundles multiple policies, the average cost is $2,441 per year, or roughly $204 per month. This package typically includes the following:

- General liability: $846 per year

- Workers’ compensation: $483 per year

- Professional liability: $709 per year

- Business Owner’s Policy (BOP): $1,249 per year

These numbers are useful benchmarks, but actual costs depend on factors like the type of equipment you own, your location, and the volume of rentals.

Experts suggest allocating 1–3% of your annual revenue for insurance expenses. For example, a business earning $100,000 annually should plan to spend $1,000 to $2,000 on coverage. Smaller operations with $50,000 in revenue might budget $500 to $1,500, while businesses pulling in $200,000 or more may approach the average bundled cost of $2,441.

The next section will explore strategies to reduce these expenses.

Ways to Lower Insurance Costs

One effective way to cut costs is by bundling policies, such as general liability, workers’ compensation, and a BOP. This approach often yields 10–20% savings. For instance, a small bounce house rental business could save around 15%, reducing total annual costs from over $3,000 to approximately $2,441.

Another cost-saving strategy involves adopting strong safety measures. Businesses that implement staff training programs, conduct regular equipment inspections, and follow ASTM-compliant safety standards can see premiums drop by 10–25%. For example, companies with documented training protocols have reported lowering their general liability costs from $800 to $600 annually.

Additionally, choosing insurers experienced with inflatable rentals can result in 5–15% savings. These providers often craft policies tailored to the industry, which include fewer exclusions. To get the best rates, always request quotes from at least three to five providers and provide detailed information about your equipment, safety practices, and location.

How to Find the Right Insurance Coverage

Evaluate Your Coverage Requirements

Understanding your specific coverage needs is a crucial first step in choosing the right insurance policy. Start by listing all your assets and potential risks. For instance, inflatables like bounce houses, obstacle courses, or water slides each carry unique risks. Don’t forget to include vehicles, storage locations, and other party equipment such as dunk tanks or concession machines in your inventory.

Think about your clientele and event locations as well. A private backyard party might require lower liability limits compared to larger events like school carnivals, city festivals, or corporate gatherings. High-profile venues often mandate higher general liability coverage, typically $1 million or $2 million. Additionally, your staffing setup matters – whether you employ staff, work with subcontractors, manage setups yourself, or deliver across state lines, all of these factors influence the type of coverage you’ll need.

Once you’ve outlined your requirements, you’ll be ready to gather customized quotes.

Get Quotes from Industry Specialists

Reach out to two to four insurance providers who specialize in your industry. These experts are familiar with the risks specific to your business and can offer policies tailored to your operations instead of generic coverage.

Have the following information ready when requesting quotes: your years in business, annual revenue, rental frequency, and a detailed inventory of your equipment, including each item’s value and age. Be prepared to share your claims history, even for minor incidents, as well as details about the types of venues you typically serve and the average crowd sizes.

When comparing quotes, don’t just focus on the annual premium. Pay close attention to the liability limits – both per occurrence and aggregate – deductibles, and whether defense costs are included within or outside the policy limits. Check which types of inflatables, event scenarios, and locations are covered. Also, confirm whether your equipment is insured during transit and while off-site.

This approach ensures you’re evaluating policies that align with your unique needs.

Check Policy Exclusions

Carefully review the full policy document, including any endorsements, to understand exclusions related to inflatables, amusement devices, water activities, and supervision requirements.

Look out for common exclusions that could leave you vulnerable. For example, some policies may deny claims for improper setup, arguing that stakes or sandbags weren’t used exactly as specified. Others might exclude unsupervised use, requiring a trained attendant or designated adult supervisor to be present. Weather-related exclusions are another critical area – some insurers won’t cover damage from "foreseeable" conditions like high winds or heavy rain, which is a major concern for outdoor rentals.

For any exclusion, ask your agent if it can be modified or added back through an endorsement. If an exclusion is non-negotiable, adjust your business practices to comply with the policy. For instance, if unsupervised use is prohibited, you may need to stop offering customer self-setup options.

Conclusion

Insurance plays a crucial role in shielding your inflatable rental business from financial ruin. Even a single accident or property damage claim could saddle a small operation with overwhelming legal and medical expenses, potentially leading to bankruptcy.

When planning your insurance budget, keep in mind that general liability coverage generally costs between $300 and $800 annually. If you opt for a more comprehensive package, expenses can range from $2,000 to $2,500 annually. Your actual premiums will depend on factors like your equipment inventory, location, safety record, and the types of events you cater to. These numbers highlight the importance of adopting strong safety measures – not just for customer protection but also to help manage costs.

In addition to securing the right insurance, focus on implementing solid safety protocols. Regular inspection logs, standardized setup procedures, and thorough employee training can go a long way in minimizing risks. Maintaining a clean claims history can also help you qualify for lower premiums. It’s a good idea to consult insurance specialists who understand the unique needs of inflatable rental businesses, as they can help you navigate policy exclusions and find the best coverage.

For businesses like Bouncy Rentals USA, which offer a wide range of inflatables – think bounce houses, water slides, dunk tanks, and even concession machines – comprehensive insurance is key to supporting long-term growth and earning client trust. Keep an accurate inventory of your equipment, document your safety measures, and shop around for quotes from industry experts before your next rental.

FAQs

What are some tips to reduce the cost of insurance for inflatable rentals?

To keep your inflatable rental insurance costs under control, start by putting strong safety measures in place. This helps reduce risks and keeps your rental history spotless. Choose coverage that matches your business needs – skip the extras you don’t require. You might also save by bundling policies, raising your deductible, or partnering with an insurer experienced in inflatable rentals. These strategies can help you cut costs without compromising the protection your business needs.

Which events usually need higher insurance coverage for inflatable rentals?

When planning large-scale events like school carnivals, community festivals, or corporate gatherings, it’s essential to consider higher insurance coverage. Events that involve alcohol or high-risk activities – think mechanical bulls or inflatable obstacle courses – carry greater liability risks. Securing additional coverage helps ensure everyone’s safety and provides valuable protection for all parties involved.

Why is general liability insurance important for inflatable rentals?

General liability insurance plays a key role in inflatable rentals, offering protection to both the rental company and its customers against unforeseen risks. If an injury or property damage occurs during an event, this type of coverage helps handle any legal or financial challenges that might arise.

With the right insurance in place, you can focus on enjoying your event, knowing that safety and interests are well-protected. It’s a simple way to ensure a worry-free experience for everyone involved.