If you’re renting or operating inflatables in Georgia, here’s what you need to know:

- State Law: Georgia does not require liability insurance for inflatables under the Amusement Ride Safety Act. However, many venues (e.g., parks, schools, churches) demand proof of insurance before use.

- Local Rules: Cities like Atlanta and counties like Fulton often require a Certificate of Insurance (COI). Check with venues for specific requirements.

- Risks: Over 2,500 U.S. injuries over the past decade have been linked to inflatables. Wind gusts as low as 20 mph can cause accidents, making insurance a smart choice. It is also vital to set up a safety perimeter to minimize physical hazards.

- Costs: Liability insurance for inflatable rentals typically starts at $1,790 annually.

While Georgia’s regulations are less strict compared to states like Texas, California, and Florida, ensuring proper insurance and safety practices is key to avoiding legal and financial issues.

1. Georgia

Regulatory Body

In Georgia, inflatable rentals fall under the oversight of the Office of the Commissioner of Insurance and Safety Fire (OCI). Through its Safety Inspection Division, this office ensures compliance, while the Georgia State Fire Marshal (GSFMO) handles licensing for traveling carnivals and circuses, along with issuing Certificates of Competency. Since July 12, 2021, all licensing and permit applications have been streamlined through the OCI Citizenserve Portal.

These regulations provide a framework for understanding how liability is managed in the state.

Minimum Liability

Georgia does not impose a statewide minimum liability requirement for inflatables. This is because inflatables, moonwalks, and similar unpowered playground equipment are specifically excluded from the Amusement Ride Safety Act. Instead, they are classified separately from regulated amusement rides.

Unique State Rules

Beyond regulatory measures, Georgia has specific operational rules for inflatables:

- Proper setup is required: On concrete or asphalt surfaces, specialized anchors and ground covers must be used. On grass, specific anchoring methods are required.

- Adult supervision is mandatory: Operators must ensure there is always an adult present to oversee the equipment.

- Power requirements: Most inflatables need access to a 110-volt household outlet within 100 feet or a generator.

For any safety-related concerns, you can reach out to the Engineering Division by phone at (404) 656-2064 or via email at Firemarshal@oci.ga.gov.

2. Texas

Texas takes a more rigorous approach compared to Georgia when it comes to regulating inflatable rentals. The Texas Department of Insurance (TDI) oversees these operations under the Amusement Ride Safety Inspection and Insurance Act (Texas Occupations Code, Chapter 2151). Inflatables powered by continuous air devices fall under the Class B amusement rides category, meaning they are regulated similarly to other amusement equipment. This classification ensures a higher level of oversight regarding liability and inspections.

Minimum Liability

Texas sets a high bar for liability coverage. Operators are required to carry a combined single limit insurance policy of at least $1 million per occurrence. The policy must come from an insurer authorized to operate in Texas, a surplus lines insurer, or through an independently procured policy. Running a business without this insurance is against the law.

Inspection Requirements

State-certified inspections are a must for every inflatable in Texas. After an inspection, operators need to fill out a detailed 10-page application, including equipment serial numbers and other specifics. Once approved, the TDI provides an official inspection sticker for each inflatable. Jamie Montelongo, owner of J&M Jumping Balloons, explains:

"Anybody that operates a business that has a bounce house that are run by a blower that’s continuous flow of air, they have to be inspected and your business has to be insured by the state before you can operate."

Operating without this sticker is considered a criminal offense, punishable by fines of up to $2,000 and up to 180 days in jail. Ben Gonzalez, spokesperson for the Texas Department of Insurance, adds:

"We have 10 days by rule to get that sticker back to them. But, generally, it doesn’t take that full 10 days. Typically, we get it back to them as soon as we can."

Unique State Rules

Texas also requires operators to report injuries, display specific signage, and keep records of any government actions involving their equipment. Customers are encouraged to check for the official TDI inspection sticker before using any inflatable.

3. California

In California, insurance requirements are determined at the local level. This means cities, counties, and venues establish their own rules, creating a patchwork of regulations similar to what’s seen in states like Texas and Florida. Event operators need to carefully navigate these localized requirements.

Minimum Liability

Most venues in California require event liability insurance with a minimum of $1 million per occurrence and $2 million aggregate, and the venue must be named as an Additional Insured. Juan Cruz, VP of Marketing & Development at Inszone Insurance Services, highlights this standard:

"Most California venues require at least $1 million per occurrence / $2 million aggregate in event liability insurance, with the venue named as an Additional Insured."

However, in cities like Los Angeles and Beverly Hills, the minimum liability can increase to $2 million per occurrence, reflecting the higher risks and costs associated with these areas. Unlike Georgia, where some venues may allow exemptions, California venues often enforce stricter requirements.

Regulatory Body

California operates under a decentralized framework, with no overarching state agency regulating event insurance. Local authorities enforce compliance by requiring event organizers to submit a Certificate of Insurance (COI) before hosting events in public spaces or venues.

Unique State Rules

California’s insurance landscape also accounts for its specific environmental risks. Wildfires and weather-resistant bounce houses and extreme conditions have led insurers to develop specialized policies for outdoor events. For example, some policies include weather-triggered riders that pay out based on measurable factors like wind speeds or air quality levels. These tailored policies aim to address the challenges posed by the state’s unique risk profile.

Additionally, venues often require the event location to be listed as an Additional Insured and may impose safety measures or inspections before granting approval. These localized and risk-specific measures highlight the complexity of operating in California and the need for careful planning when organizing events.

4. Florida

Florida, much like California, handles inflatable insurance through localized regulations. However, its rules are shaped by distinct local needs. Instead of a uniform state-wide policy, Florida allows municipalities, schools, parks, and venues to set their own requirements for liability coverage.

Minimum Liability

In Florida, most venues require operators to carry liability insurance and often insist on being listed as an additional insured on the policy. This applies to a variety of locations, including schools, parks, and churches, though the specific coverage levels depend on the venue and its policies.

Regulatory Body

Unlike states with centralized oversight, Florida relies on local authorities and venues to enforce compliance with insurance requirements. This decentralized system mirrors California’s approach but is tailored to Florida’s unique conditions. For instance, cities like Fort Lauderdale may require operators to obtain specific permits or licenses before setting up inflatables. This means operators must check with each municipality where they plan to work to ensure they meet all local rules.

Unique State Rules

Florida’s weather is notoriously unpredictable, so venues often require operators to actively monitor weather conditions and have trained attendants on-site to enforce safety protocols. This focus on operational safety highlights how Florida prioritizes risk management to address its environmental challenges.

Advantages and Disadvantages

Georgia vs Other States Inflatable Insurance Requirements Comparison

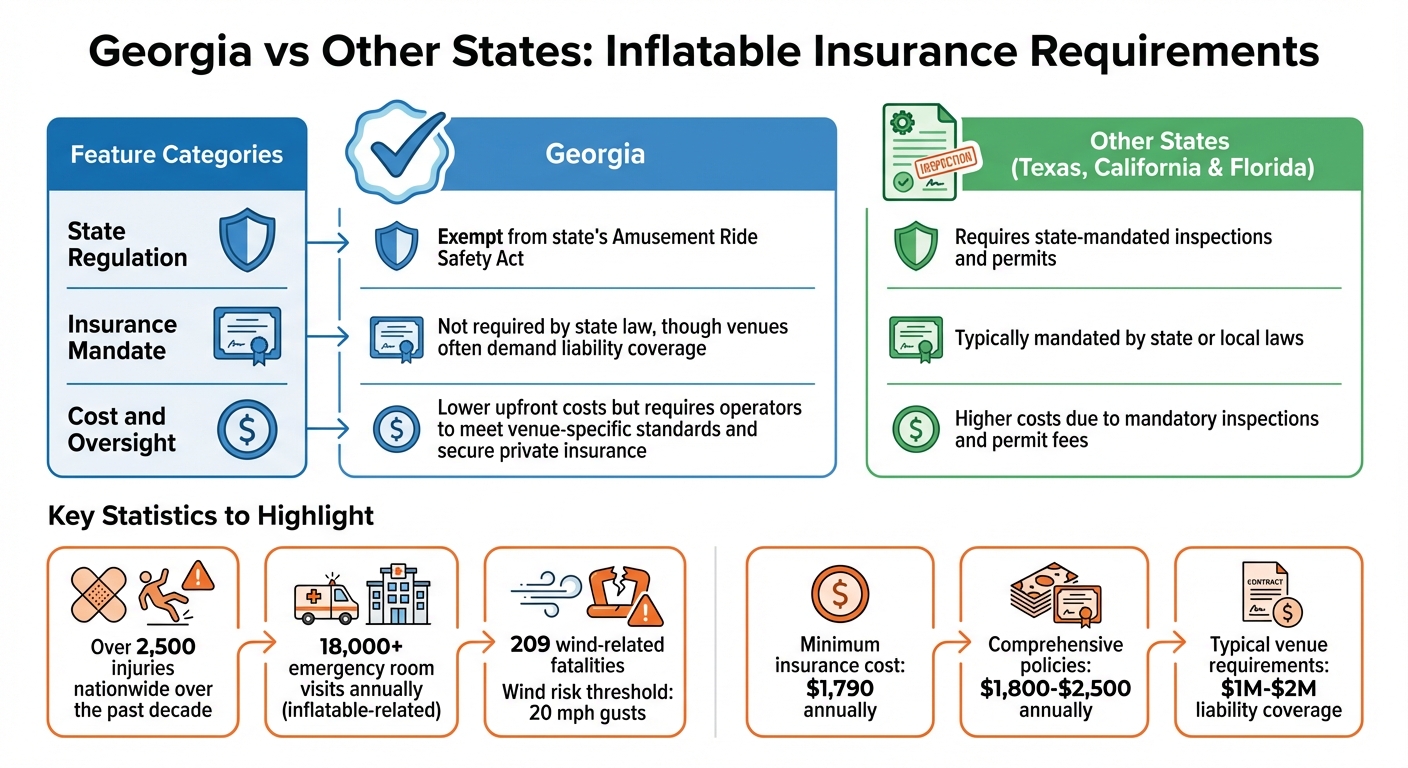

Each state’s approach to regulating inflatables brings unique challenges and benefits for rental operators. In Georgia, inflatables are exempt from the state’s Amusement Ride Safety Act, which reduces upfront costs. However, this also means operators must navigate varying local requirements on their own. Comparing Georgia’s framework with regulations in states like Texas, California, and Florida highlights these differences.

Here’s a breakdown of how Georgia stacks up against other states:

| Feature | Georgia | Other States (Texas, California & Florida) |

|---|---|---|

| State Regulation | Exempt from the state’s Amusement Ride Safety Act | Requires state-mandated inspections and permits |

| Insurance Mandate | Not required by state law, though venues often demand liability coverage | Typically mandated by state or local laws |

| Cost and Oversight | Lower upfront costs but requires operators to meet venue-specific standards and secure private insurance | Higher costs due to mandatory inspections and permit fees |

In Georgia, operators face a unique burden of proving their credibility. Without state-issued permits, they must demonstrate compliance with local safety standards, especially for venues like schools and parks. Many facilities still insist on liability coverage ranging from $1 million to $2 million. Adding to the complexity, Georgia’s frequent thunderstorms from May through September force operators to enforce strict weather policies to avoid insurance exclusions tied to wind damage.

Liability insurance remains a critical safeguard for both operators and customers. According to the U.S. Consumer Product Safety Commission, inflatable-related injuries result in over 18,000 emergency room visits each year. For new businesses, insurance costs can be a significant expense, with minimum premiums starting at around $1,790 and comprehensive policies ranging from $1,800 to $2,500 annually.

For companies like Bouncy Rentals (https://bouncyrentalsusa.com/), maintaining full insurance coverage and following strict safety protocols is a priority. This commitment helps build trust with clients, even in states like Georgia, where regulatory oversight varies widely.

Conclusion

Georgia’s exemption from the Amusement Ride Safety Act creates a distinct operating environment for inflatable rentals. Without mandatory state inspections or permits, operators benefit from lower initial costs. However, many venues and local jurisdictions still require proof of liability insurance, making it a critical operational consideration. This unique setup demands that operators fully understand the financial risks and safety responsibilities they face.

Nationwide data highlights the stakes: over 2,500 injuries and 209 wind-related fatalities emphasize the importance of liability insurance. Not having adequate coverage could leave your business vulnerable to lawsuits and medical claims that far exceed the typical annual premium of around $1,790. As Titan Inflatables warns:

"Without proper insurance, your business could face costly lawsuits, medical expenses, and legal fees, which could potentially bankrupt your operation."

Unlike states with stricter regulations, Georgia’s more relaxed framework shifts the responsibility for safety and insurance onto the operators. To succeed, businesses should treat insurance as a cornerstone of their operations. This includes verifying local permit requirements, ensuring policies name venues as additional insured, and implementing strict weather protocols. Liability waivers for every rental also strengthen legal protection. These proactive measures are particularly important in Georgia’s varied regulatory landscape.

The lack of state oversight means operators must take full ownership of maintaining high standards. Comprehensive insurance, strong safety practices, and a commitment to professionalism are essential for building a trustworthy reputation. Companies like Bouncy Rentals (https://bouncyrentalsusa.com/) exemplify how prioritizing insurance and safety can foster client confidence, even in a state with minimal regulations. In Georgia, managing insurance carefully and maintaining rigorous safety protocols aren’t just best practices – they’re essential for protecting your business and ensuring long-term success.

FAQs

What coverage limits do Georgia venues usually require?

Most venues in Georgia mandate inflatable rental insurance with coverage limits of at least $1 million per occurrence and $2 million in general aggregate coverage. These requirements are in place to provide sufficient protection for both the renters and the venues during events.

What should a Georgia COI include for inflatables?

A Georgia Certificate of Insurance (COI) for inflatables needs to confirm that the required insurance coverage is in place, as mandated by state regulations. This document should clearly outline liability coverage to safeguard against potential bodily injury or property damage claims. It’s crucial to verify that the COI adheres to all legal requirements to ensure compliance and operate lawfully within Georgia.

When should inflatables be shut down for wind in Georgia?

Inflatables in Georgia should be taken down when wind speeds hit 15-20 mph to maintain safety. It’s crucial to keep a close eye on weather conditions while they’re in use, as safety should always come first.