Running a bounce house rental business in Florida involves risks like injuries, property damage, and weather-related incidents. Without insurance, a single accident could lead to financial disaster. Here’s what you need to know:

- Why You Need Insurance: Protects your business from lawsuits, covers medical costs, and is often required by venues like parks and schools.

- Florida Requirements: No statewide mandate, but public venues typically require liability insurance, often with $1M per incident and $3M aggregate coverage.

- Types of Coverage:

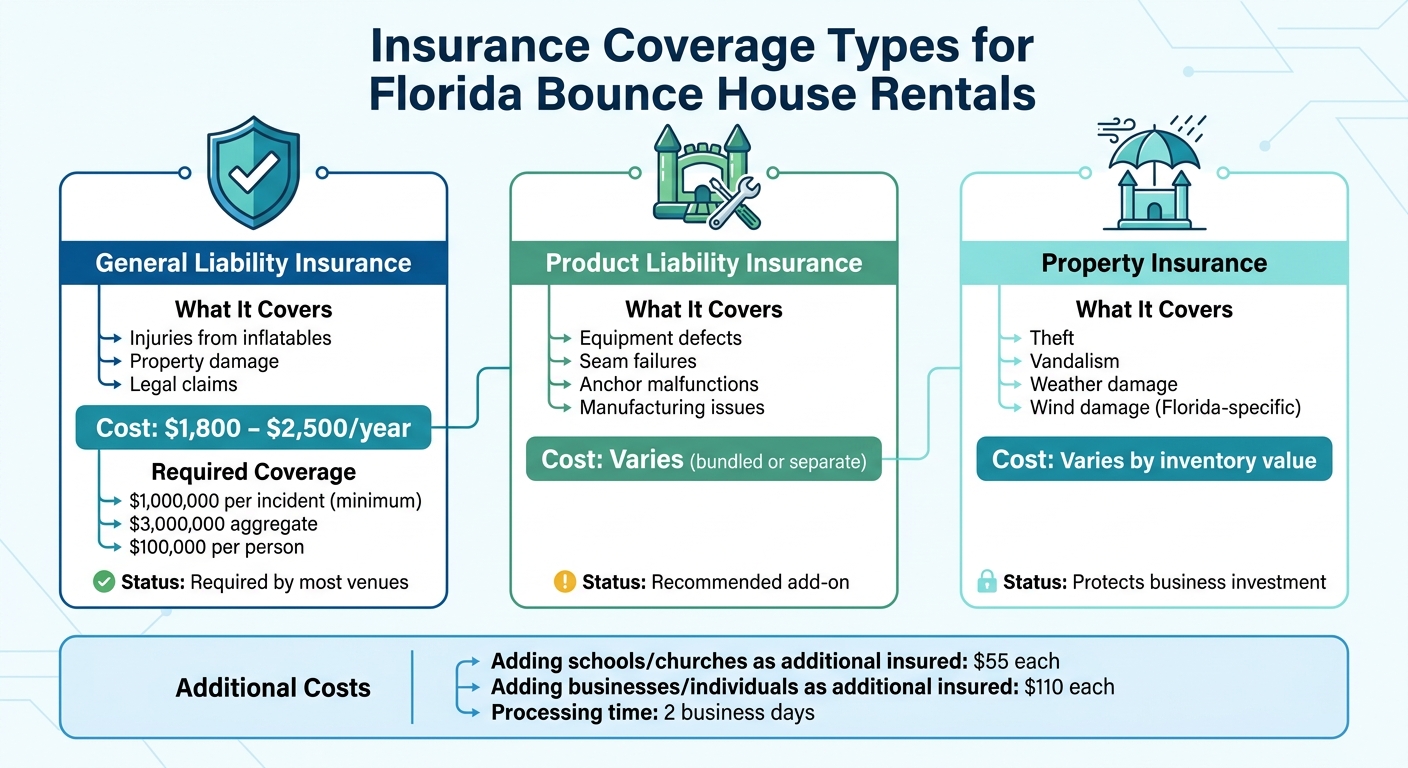

- General Liability: Covers injuries and property damage.

- Product Liability: Protects against equipment defects.

- Property Insurance: Covers theft, vandalism, and weather damage.

- Costs: General liability policies for inflatables range from $1,800 to $2,500 annually. Adding venues as "additional insured" costs $55–$110.

- How to Get Covered: Use specialized insurers, compare quotes, and ensure policies meet venue requirements.

To stay compliant, update your policy annually, follow safety protocols, and keep Certificates of Insurance ready for venue requests.

Florida Insurance Requirements for Bounce Rentals

In Florida, there isn’t a single statewide law mandating insurance for bounce house businesses. Instead, the need for insurance often depends on the venue or property owner. Public parks, schools, churches, and municipal facilities almost always require proof of liability insurance before allowing equipment to be set up.

Many venues also require being added as "additional insured" on your policy, which protects them in case of an incident. Adding a city, church, or school to your insurance typically costs $55 each, while private businesses or individuals cost $110. Keep in mind, processing these certificates takes about two business days, so it’s wise to plan ahead for public events. A typical liability policy for rental companies includes $3 million in aggregate coverage, $1 million per incident, and $100,000 per person. These coverage levels are generally required for public venues.

For private backyard events, insurance isn’t legally required for residential properties. However, it’s strongly recommended to shield your business from potential personal liability claims. The real challenges arise when operating in public spaces. Renting out equipment at parks or other public areas requires partnering with a company that has the necessary insurance coverage.

Since requirements can vary by location, some municipalities might also ask for specific permits or safety inspections in addition to insurance certificates. It’s always a good idea to contact the local parks department or venue directly to confirm their standards. What works in Miami might not meet the rules in Tampa or Jacksonville.

Types of Insurance Coverage for Inflatable Rentals

Florida Bounce House Insurance Coverage Types and Costs Comparison

If you’re running a bounce house rental business, understanding the right insurance policies is crucial. Not only does proper coverage keep your business protected, but it also ensures you meet venue requirements. In Florida, many operators rely on a mix of policies to cover various risks. Here’s a closer look at the key types of insurance you’ll need.

General Liability Insurance

General liability insurance is the backbone of your coverage. It’s designed to protect your business from claims related to injuries or property damage caused by your inflatables. For example, if someone is injured while using your equipment or if a bounce house accidentally damages property, this policy steps in. Given that most Florida venues require proof of liability insurance, having a policy with at least $1,000,000 in coverage is a smart move.

On average, small business general liability insurance costs around $1,057 per year. However, specialized policies tailored to inflatables typically range from $1,800 to $2,500 annually. This investment ensures you’re prepared for the unexpected while meeting venue standards.

Product Liability Insurance

Product liability insurance is specifically designed to address issues stemming from defects in your equipment. Think of scenarios like a seam splitting or an anchor failing – these aren’t always covered under general liability policies. This type of insurance adds an extra layer of protection against claims resulting from faulty or malfunctioning equipment.

Property Insurance

Your inflatables are a big investment, and property insurance helps protect that investment. This policy covers risks such as theft, vandalism, and damage caused by weather. Whether your equipment is in storage or actively being used at an event, property insurance ensures you’re not left footing the bill for unexpected losses.

In Florida, where hurricane season brings unique challenges, it’s especially important to confirm your policy includes coverage for wind damage and other location-specific risks. This attention to detail can make all the difference in keeping your business running smoothly, even after unforeseen events.

How to Get Insurance Coverage for Your Florida Bounce Rental Business

Once you’ve figured out what coverage you need, the next step is securing a specialized policy. This is no small task – bounce house businesses come with unique risks, and many standard insurers won’t even consider covering them. Here’s how you can navigate the process efficiently and get the right coverage for your business.

Find Insurance Providers That Cover Inflatable Rentals

Skip your usual insurance agent. Most standard providers don’t cover inflatable rentals. Instead, search for specialized providers using terms like "inflatable jumper rental insurance", "bounce house liability", or "party rental business owner insurance". These keywords can help you find companies that truly understand the risks tied to your industry.

"Inflatable and bounce house rental businesses face unique liability exposures… many inflatable operators struggle to find coverage through standard markets."

Focus on providers with experience in amusement industry insurance, especially those connected to groups like the International Association of Amusement Parks and Attractions. Be cautious of companies offering instant online quotes without reviewing your equipment or business operations. Instead, schedule a consultation to go over your inventory – whether you rent supervised or unsupervised units – and your delivery processes. Also, make sure the provider can issue Certificates of Insurance (COIs) that meet Florida’s requirements, such as listing venues as additional insured.

Get and Compare Multiple Quotes

Once you’ve identified a few potential insurers, request quotes from at least three specialized providers. Don’t just look at the premium – dig into the details. Check for coverage options like participant accident coverage and general liability, which together can reduce your overall risk. Ask whether the provider charges for additional insured certificates. For example, some Florida providers charge $55 for schools or churches and $110 for businesses or individuals.

Policy flexibility is another key factor. Can you add new inflatables or concession equipment mid-term as your business expands? This is important to ensure your coverage grows with your inventory. Also, read the fine print for any exclusions – some policies won’t cover certain items like water slides or mechanical bulls. Finally, confirm whether the provider offers 24/7 online access to print COIs, so you’re prepared when venues request them on short notice.

Check Policy Terms and Coverage Limits

Before you finalize anything, double-check that your policy meets the insurance requirements of the venues where you’ll operate. Most venues require limits around $1 million per incident and $2 million aggregate, although some municipalities may ask for $3 million in aggregate coverage.

Be sure your policy also aligns with your business model, whether you handle indoor or outdoor setups, customer pickups, or delivery-only rentals. Some insurers may require specific contract language or offer waivers to keep your coverage valid.

Complete Your Policy Purchase

Once you’ve chosen a provider, you’ll need to submit the necessary paperwork to finalize your policy. This typically includes details about your business structure, equipment inventory, and operational procedures. Keep in mind that specialized policies often go through an underwriting review before they’re approved.

Make sure your coverage is active before taking any bookings. Also, secure digital copies of your policy documents and COIs right away, so you’re ready to provide proof of insurance when needed.

Staying Compliant and Maintaining Safety Standards

Insurance is just the beginning – keeping your business safe and compliant requires regular policy updates, strict safety protocols, and proper documentation.

Update Your Policy Annually

Take time to review your insurance policy every year. As your business grows and you invest in new equipment – like inflatables, obstacle courses, tents, or concession machines – make sure your policy reflects these changes. Many insurance providers allow mid-term updates to add new items, which may adjust your premium accordingly. If you expand your inventory, update your policy immediately to ensure all new equipment is covered.

Keeping your coverage up to date is only part of the equation. Pair it with strong safety practices to protect your business.

Follow Safety Procedures

While insurance provides financial protection, following safety procedures can help you avoid incidents altogether. Active supervision is crucial, as lack of oversight is a leading cause of injuries. Weather conditions are another major factor – wind-related accidents alone have resulted in approximately 209 deaths. Set clear protocols for shutting down operations during unsafe weather, especially in high winds.

Also, keep detailed records of equipment maintenance and setup. These logs can serve as evidence against negligence claims. Together, these practices not only reduce risks but also ensure compliance with venue safety standards.

Supply Certificates of Insurance When Needed

Beyond maintaining safety and updating policies, many venues in Florida – such as schools, parks, and municipalities – require proof of insurance before allowing rentals on their property. Make sure your insurance provider offers 24/7 access to Certificates of Insurance (COIs) so you can provide verification quickly when requested.

"Many venues require a COI before renting inflatables".

Additionally, confirm that your insurer can name third parties as additional insureds. This feature is often a requirement for securing contracts with high-profile clients like cities and school districts, which typically have strict vendor insurance policies.

Conclusion

When running a bounce rental business in Florida, it’s crucial to understand the state’s specific requirements and the risks unique to your industry. These risks can range from participant injuries to equipment damage and property liability. To address these, you’ll need tailored insurance coverage, including General Liability, Product Liability, and Property Insurance.

Once you’ve identified your coverage needs, the next step is finding insurance providers that specialize in inflatable rentals. Gather multiple quotes and carefully evaluate the coverage limits, exclusions, and costs. Before committing to a policy, ensure it aligns with Florida’s regulations and meets the expectations of your clients, especially if you’re working with schools, municipalities, or corporate clients that require proof of insurance.

Insurance isn’t something you can set and forget. Always keep Certificates of Insurance on hand for venue requirements, and prioritize strict safety measures to reduce the likelihood of incidents. These practices not only protect your finances but also open doors to high-value contracts with organizations that demand vendor insurance as a prerequisite.

"Protecting your assets, having a cash cushion and strong cash flow, and insuring your business against everything from employee injuries to property damage are all key elements in growing your party rental business for long-term success." – Big & Bright Inflatables

This advice underscores the importance of comprehensive insurance coverage in securing your business’s future. By meeting Florida’s venue requirements, you not only stay compliant but also position your business to land lucrative contracts. Solid insurance coverage safeguards your operations from financial setbacks and ensures a safe, professional experience for your clients. Taking these steps lays the groundwork for long-term success and credibility in Florida’s competitive bounce rental market.

FAQs

What should I do if a venue asks for higher limits than my policy?

If a venue asks for higher insurance limits than your policy currently offers, you can work with your insurer to adjust your coverage. You might choose to raise your policy limits or buy a separate excess or umbrella policy to meet the requirements. Make sure to double-check with your insurer that the updated limits are in place and that your coverage still aligns with your business needs.

Will my insurance still cover me if a customer sets up the inflatable themselves?

When customers set up inflatables themselves, insurance coverage might not apply. Many policies specifically require that insured, trained personnel handle the setup to ensure safety and meet liability standards. It’s important to check the exact terms of your policy to avoid any potential coverage problems.

What exclusions should I watch for (like water slides or wind incidents)?

When insuring inflatable rentals, it’s crucial to look out for exclusions in your policy. For instance, water slides might not be covered, or the policy may only include specific types of inflatables. Another common exclusion is wind-related incidents, particularly for outdoor setups that aren’t properly secured. To avoid surprises, thoroughly review your policy to understand what’s covered – especially for weather or water-related risks – and always ensure inflatables are securely anchored to reduce potential hazards.