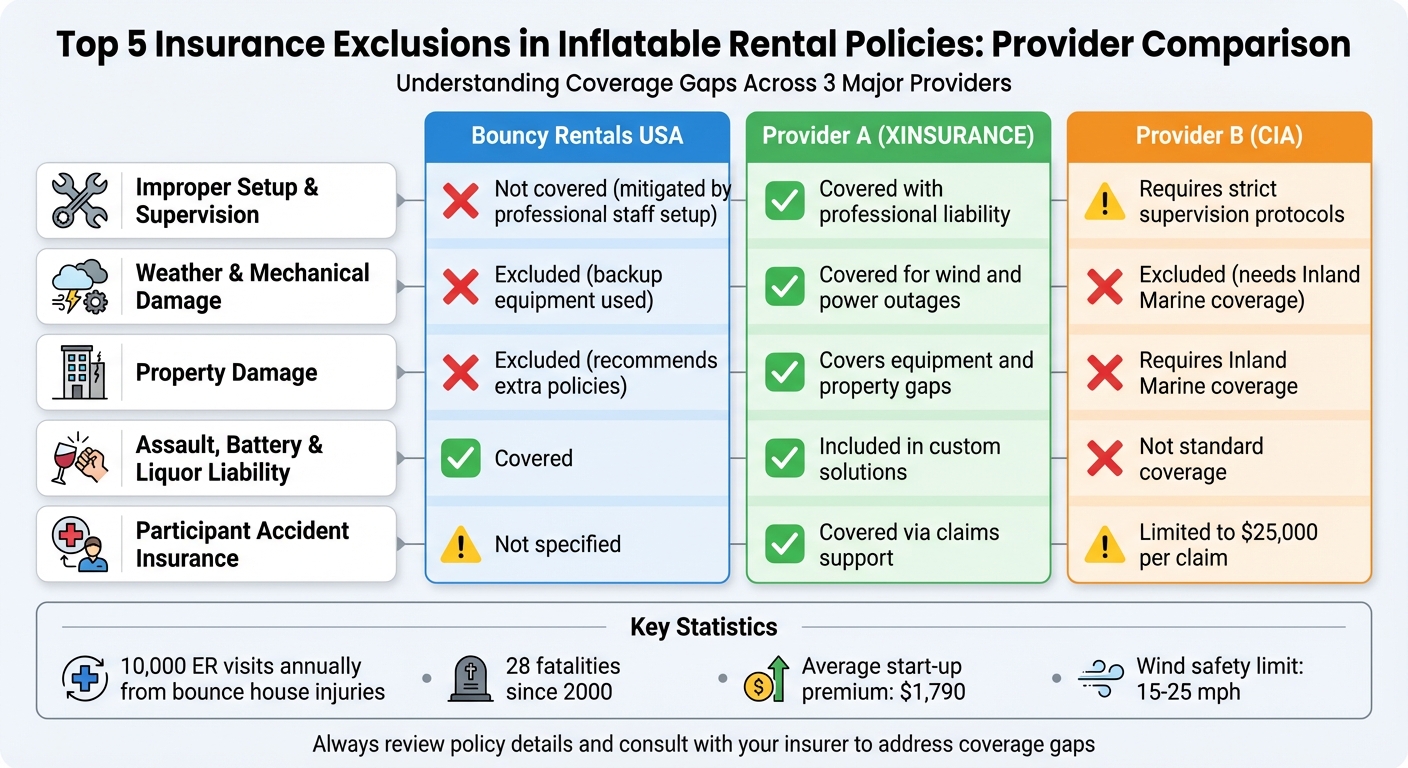

When running an inflatable rental business, insurance is essential to protect against accidents and liabilities. However, many policies have exclusions that can leave you exposed to significant risks. Here are the top five exclusions you need to know:

- Improper Setup and Supervision: Claims from incorrect installation or lack of supervision are often not covered. For example, if a bounce house isn’t securely anchored or no adult monitors it, your policy may deny the claim.

- Weather and Mechanical Damage: Damage caused by high winds, storms, or equipment failures like deflating bounce houses is typically excluded. Monitoring weather and having backup equipment can help mitigate these risks.

- Property Damage: Standard policies exclude damage to rented venues or the inflatables themselves. Additional coverage, such as "Equipment Rental Liability" or "Property Coverage", may be needed.

- Assault, Battery, and Liquor Liability: Events involving alcohol or incidents like fights often aren’t covered by basic policies. Specialized policies can address these gaps.

- Participant Accident Insurance: Injuries to users may not be fully covered under general liability. Separate accident insurance can help cover medical costs.

Quick Comparison

| Exclusion Type | Bouncy Rentals USA | Provider A (XINSURANCE) | Provider B (CIA) |

|---|---|---|---|

| Improper Setup/Supervision | Not covered; mitigated by staff setup | Covered with professional liability | Requires strict supervision |

| Weather/Mechanical Damage | Excluded; backup equipment used | Covered for wind and power outages | Excluded; needs Inland Marine |

| Property Damage | Excluded; recommends extra policies | Covers equipment and property gaps | Requires Inland Marine coverage |

| Assault & Battery | Covered | Included in custom solutions | Not standard |

| Participant Accident Insurance | Not specified | Covered via claims support | Limited to $25,000 per claim |

Understanding these exclusions and securing additional coverage where needed can safeguard your business from unexpected financial burdens. Always review your policy details and consult with your insurer to address potential gaps.

Inflatable Rental Insurance Exclusions: Provider Coverage Comparison

1. Bouncy Rentals USA

At Bouncy Rentals USA, protecting our business with the right insurance is a top priority. While our policy offers robust protection, there are specific exclusions every business owner should be aware of. Let’s break down the key areas not covered and how we work to minimize these risks.

Improper Setup and Supervision

Claims stemming from improper installation or setup of inflatable units are not covered under our policy. For example, if a bounce house isn’t securely anchored and someone gets hurt, the claim could be denied. Similarly, incidents that occur without adequate adult supervision also fall outside of coverage. Operational mistakes, like setup errors, aren’t included in general liability protection either. To address this, we take full responsibility for all setup and takedown, ensuring everything is done correctly and safely.

Weather and Mechanical Damage

Our policy doesn’t cover damages caused by severe weather or mechanical failures. For instance, if strong winds move an inflatable and cause injuries, the costs for repairs or medical bills could fall on the business owner. Similarly, mechanical issues, like a generator failing and causing a bounce house to deflate, are often excluded from basic insurance plans. To reduce these risks, we keep a close eye on weather conditions and always have backup equipment ready at events.

Property Damage Exclusions

Standard policies often include a "Property in Your Care, Custody, or Control" exclusion. This means damage to rented venues or the inflatable units themselves isn’t typically covered by general liability insurance. To fill these gaps, specialized policies like "Equipment Rental Liability" can cover issues like theft or equipment malfunctions, while "Property Coverage" can help with weather-related damage or vandalism. Knowing these limitations is especially important when setting up at schools, parks, or private properties.

In the next section, we’ll compare these exclusions with other providers to showcase how we manage risks effectively.

2. Provider A

Provider A, offered by XINSURANCE, focuses on filling the gaps left by standard policies. Many traditional insurers exclude key scenarios, leaving businesses exposed. Provider A takes a different approach, offering coverage tailored to the unique risks faced by inflatable rental operators. Here’s a closer look at how they tackle critical exclusions.

Weather and Mechanical Damage

Basic policies often fall short when it comes to unpredictable weather or equipment issues. Provider A steps in with coverage for incidents like high winds that can dislodge inflatables or power outages – dubbed "Birthday Party Blackouts" – that cause sudden deflations. These protections ensure businesses are prepared for events that could otherwise derail operations.

Property Damage Exclusions

Building on their weather-related protections, Provider A also addresses property damage risks. Many standard policies include a "Property in Your Care, Custody, or Control" exclusion, which leaves businesses vulnerable. Provider A counters this by offering:

- Equipment Rental Liability: Covers malfunctions or theft of rented equipment.

- Property Coverage: Protects against weather damage, vandalism, and theft.

- "After-Dark Damage": Specifically covers vandalism or theft that occurs after business hours.

This comprehensive package ensures businesses are protected, even in scenarios that traditional policies overlook.

"You want TRU insurance, the kind that sticks by you no matter what – because when what can happen, happens, you want someone who’ll stand and fight with you, not leave you in the lurch."

– Rick J Lindsey, President and CEO, XINSURANCE

Liquor and Assault Liability

Provider A also provides coverage for assault, battery, and liquor liability – areas where standard policies often fall short. This is particularly important for events involving alcohol, as it shields businesses from claims that could otherwise be denied. Additionally, they include coverage for negligent exposure to communicable diseases, addressing a growing concern that most traditional insurers exclude.

3. Provider B

Provider B, represented by Cossio Insurance Agency (CIA), focuses on addressing common gaps in inflatable rental insurance. While standard General Liability policies cover injuries to third parties, they don’t extend to protecting the equipment itself. To fill this gap, CIA highlights the need for a separate Inland Marine policy. This type of policy safeguards inventory against risks like fire, theft, or vandalism, with premiums based on the total value of the equipment inventory.

Improper Setup and Supervision

Proper setup and supervision play a critical role in maintaining insurance coverage. CIA points out that poor supervision is one of the primary reasons claims are filed in the inflatable rental industry. Operators must ensure staff are adequately trained to manage occupancy and enforce safety rules. For instance, supervising inflatable slides requires a responsible adult (not a teenager) to monitor and enforce the "one-at-a-time" rule at all times.

Liquor Liability

Alcohol-related risks are a significant concern for CIA. To mitigate these risks, the agency excludes coverage for mechanical bulls at events where alcohol is served. This measure is designed to reduce liability stemming from incidents involving intoxicated participants.

Weather and Mechanical Damage

Using weather-resistant bounce houses can help, as weather conditions are a significant risk factor for inflatable rentals. For example, wind gusts as low as 20 mph can lift a bounce house off the ground, posing serious safety risks. Budget insurance policies often exclude coverage for weather-related damage. CIA advises operators to monitor weather forecasts daily and avoid operating equipment when wind speeds exceed the manufacturer’s recommended limits, typically between 15 to 25 mph.

As of February 2019, the average minimum premium for start-up inflatable rental businesses was around $1,790.

Property Damage Exclusions

Standard insurance policies include a "Care, Custody, and Control" exclusion. This means that damage to rented venues or the inflatables themselves isn’t covered under basic liability policies. To address this gap, CIA recommends Inland Marine coverage. This policy protects businesses from losses like theft or fire damage to their equipment, while General Liability continues to cover third-party injuries.

Coverage Strengths and Weaknesses

Looking at the provider reviews above, here’s a breakdown of key strengths and weaknesses in coverage among different providers. Insurance providers handle exclusions in various ways. For instance, Bouncy Rentals USA ensures its equipment is fully covered and collaborates with comprehensive carriers. On the other hand, specialized providers like XINSURANCE offer tailored solutions to address gaps often found in budget-friendly policies. Unfortunately, standard carriers often leave operators vulnerable to significant risks.

Here’s a quick comparison of how the providers stack up:

| Exclusion Type | Bouncy Rentals USA | Provider A (XINSURANCE) | Provider B (CIA/LiveRate) |

|---|---|---|---|

| Improper Use/Setup | Covered through comprehensive GL with trained staff protocols | Covered via "TRU Insurance" and Professional Liability solutions | Requires strict supervision; Participant Accident Insurance covers medical costs up to $25,000 |

| Weather Damage | Equipment protected; operations cease at 15–20 mph winds | Covers "wild weather" incidents that tear inflatables from anchors | Excluded in budget policies; requires separate Inland Marine coverage |

| Assault & Battery | Covered under comprehensive liability protection | Specifically included in custom solutions | Not explicitly listed as standard inclusion |

| Property Damage (Care, Custody, Control) | Equipment fully insured during transit and setup | Addressed through customized gap-filling coverage | Requires a separate Inland Marine policy as basic GL policies typically exclude equipment damage |

| Medical Payments | Included in comprehensive coverage | Handled via Claims Direct Access for proactive advocacy | $10,000 maximum benefit with a $100 deductible |

Each provider has its strengths and focus areas. For instance, XINSURANCE is known for addressing exclusions that standard policies typically ignore. As Rick J. Lindsey, President and CEO of XINSURANCE, puts it:

"Opting for cheap insurance might seem financially prudent until you face a claim that exposes the gaping holes in coverage"

Their "TRU Insurance" solutions are specifically designed to cover issues like improper use, assault and battery, and weather-related incidents – three of the most common claims in the inflatable rental industry.

One major issue with standard policies is the exclusion of equipment damage. Basic liability often doesn’t cover damage to inflatables themselves, leaving operators needing separate Inland Marine policies to protect against theft, fire, or vandalism.

Participant Accident Insurance is another valuable tool, processing claims in about a month and helping to stabilize premiums. Alex Cossio, Area Vice President at Replacement Services, explains:

"acts as a ‘sacrificial lamb’ to prevent claims against the general liability policy"

This strategy helps operators avoid steep premium hikes caused by open liability claims.

This comparison highlights the importance of understanding coverage gaps and choosing the right policies to safeguard equipment and events effectively.

Conclusion

Understanding insurance exclusions is crucial to shielding your business from potential financial disasters. Consider this: every year, around 10,000 people require emergency room treatment due to bounce house-related injuries, and 28 fatalities have been reported since 2000. These figures highlight just how high the stakes are. A single incident could lead to overwhelming medical bills, legal expenses, and settlements that could cripple an uninsured business.

The comparisons earlier emphasize why having robust coverage is so important. Cheaper policies often leave out key protections, like coverage for assault, battery, or weather-related incidents – gaps that could cost you dearly. As Rick J. Lindsey, President and CEO of XINSURANCE, puts it:

"Don’t let saving a few bucks now lead to losing a lot later"

The difference between a $300 bare-bones policy and a comprehensive $1,800 one could be the difference between weathering a claim and shutting down for good.

For businesses like Bouncy Rentals USA, which prioritize safety and full coverage, taking proactive steps can make all the difference:

- Review waivers with your insurer to ensure compliance with local safety laws and policy requirements.

- Verify product liability insurance with manufacturers before purchasing equipment.

- Request Certificates of Insurance early and add venues as "Additional Insured" at least 7–14 days before events.

- Keep detailed records of equipment maintenance, safety training, and setup protocols (including a sanitization checklist) to strengthen your defense against claims and possibly lower premiums.

- Set reminders 30–60 days before your policy expires to avoid lapses, especially during busy seasons.

These steps not only help protect your business but also demonstrate your commitment to safety and professionalism.

FAQs

What add-on policies cover excluded inflatable damage?

Add-on policies that address excluded inflatable damage often come with a range of protections, including comprehensive liability and accident coverage. These policies are designed to safeguard against claims involving bodily injury, property damage, or harm to the inflatables themselves. It’s a smart move to review your coverage details with your provider to ensure it aligns with your business requirements.

What wind speed should I stop operating inflatables?

Inflatables are not safe to use when wind speeds exceed 15 mph. If winds hit or go beyond this threshold, it’s crucial to act quickly: clear all participants, deflate the inflatable, and secure it right away to prevent accidents. Safety should always come first.

How do I avoid claim denial for setup or supervision?

To avoid claim denial, make sure inflatables are placed on a flat, stable surface and are securely anchored in line with safety standards. Maintain records of permits, insurance policies, and proof of compliance with local regulations. While the inflatables are in use, ensure proper supervision and strictly enforce safety rules to minimize accidents. Careful setup and vigilant monitoring play a crucial role in reducing risks and protecting against denied claims.