Inflatable rentals are fun but come with serious risks. Without proper liability insurance, rental businesses and event organizers could face steep costs from injuries, lawsuits, or property damage. Here’s what you need to know:

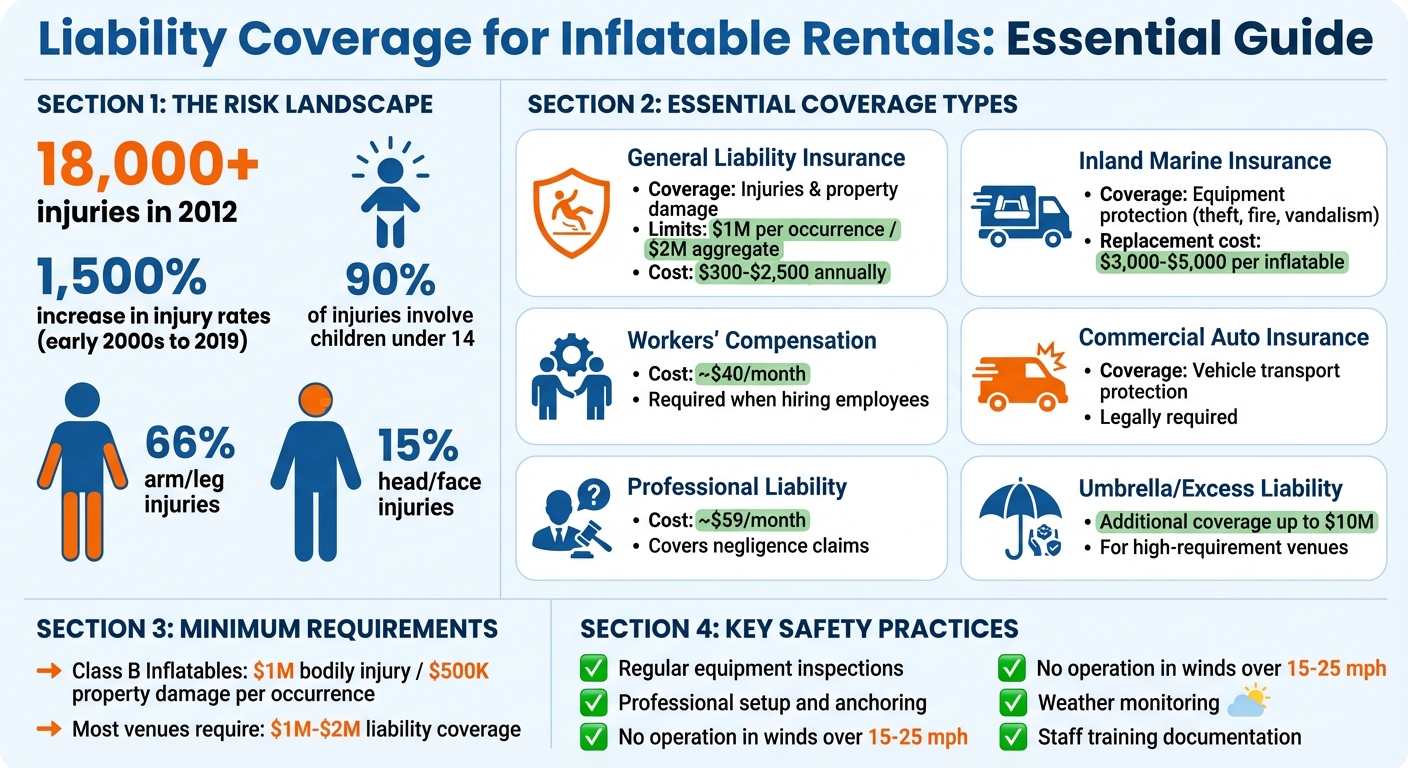

- Accident Statistics: Over 18,000 injuries were linked to inflatables in 2012, with a 1,500% rise in injury rates between the early 2000s and 2019. Most involve children under 14, with injuries like broken bones and concussions.

- Insurance Types: Key coverages include General Liability (covers injuries and property damage), Inland Marine (protects equipment like bounce houses), and optional policies like Workers’ Compensation and Commercial Auto.

- Coverage Costs: General liability premiums range from $300 to $2,500 annually, depending on business size and risk level.

- Safety Practices: Regular equipment inspections, thorough sanitization, proper setup, and adherence to weather guidelines (e.g., no operation in winds over 15–25 mph) reduce risks.

Proper insurance not only protects businesses but also ensures venues and participants are covered in case of accidents. Companies like Bouncy Rentals USA combine full insurance with rigorous safety measures to create a secure experience for all.

Inflatable Rental Insurance Coverage Types and Costs Guide

Risks Associated with Inflatable Rentals

Common Hazards with Inflatable Equipment

Inflatable rentals come with a range of safety challenges that can lead to serious injuries. One of the most frequent issues is collisions, especially when children of different ages and sizes share the same inflatable. Statistics show that nearly 90% of injuries from inflatable accidents involve individuals aged 14 or younger, with about two-thirds of these injuries affecting the arms and legs, and 15% involving the head or face. Notably, over 90% of injuries in inflatable amusements are tied to moon bounces.

Weather-related incidents are another major concern. High winds can cause inflatables to tip over, become airborne, or even drift into traffic if they’re not securely anchored. Manufacturers typically recommend avoiding operation in wind speeds over 15 to 25 mph, as these conditions exceed safety limits. Rain also adds risks by making surfaces slippery, increasing the chances of falls and collisions. These weather-related dangers highlight the importance of having strong liability coverage to handle potential claims.

Equipment failures are equally alarming. Sudden deflation or collapse can lead to entrapment, putting participants at significant risk. These failures often stem from issues like malfunctioning blowers, worn-out cords, or punctured vinyl. Such problems not only endanger users but can also lead to lawsuits for bodily injury or property damage. These hazards underline the importance of proper maintenance and inspection to mitigate risks.

Financial Costs of Liability Claims

Accidents involving inflatables can have a severe financial impact on rental businesses. Medical expenses for treating injuries such as fractures, concussions, or more severe conditions like paralysis can add up quickly. Beyond medical costs, businesses may face significant legal expenses, including defense fees, settlements, and potential payouts from lawsuits – any of which can threaten the survival of the business.

Property damage adds another layer of financial risk. Rental companies may need to cover repair or replacement costs for client property damaged during setup or due to equipment malfunctions. On top of that, the company’s own assets are at risk from events like fire, theft, or vandalism, potentially resulting in lost income or the need for costly equipment replacements. To help mitigate these risks, Class B inflatables are required to carry minimum liability limits of $1,000,000 for bodily injury and $500,000 for property damage per occurrence.

Types of Liability Coverage for Inflatable Rentals

General Liability Insurance

If you’re running an inflatable rental business, Commercial General Liability (CGL) insurance is a must-have. This coverage protects you from third-party claims involving injuries or property damage that might occur during a rental period. Think of it as your first line of defense in case something goes wrong.

Most CGL policies come with limits like $1,000,000 per occurrence and $2,000,000 general aggregate – essentially, that’s the maximum payout for a single incident and for all claims during your policy period. It also covers legal defense costs, which can add up quickly. For small operations, annual premiums usually fall between $1,800 and $2,500, though some businesses report paying as little as $300 to $1,500, depending on their size and risk level.

"General liability insurance is non-negotiable for bounce house operators, as children’s activities combined with inflatable equipment create an environment where injuries, though hopefully rare, are a legitimate concern." – Got Inflatables

Many venues, like schools and parks, won’t allow you to set up unless you provide proof of insurance. They may also require you to list them as an "Additional Insured" on your policy. Without this coverage, you’re personally responsible for medical bills, legal fees, and settlements if something goes wrong. It’s an essential layer of protection for any rental business.

Next, let’s talk about protecting your equipment itself.

Commercial Property Insurance

While general liability covers injuries and damages to others, Inland Marine Insurance is what keeps your equipment safe. This type of policy protects your inflatables from risks like theft, fire, or vandalism while they’re in transit or at a customer’s location. Standard property insurance, in contrast, only covers items stored at your warehouse.

Inflatables are often used off-site, which makes Inland Marine coverage crucial. For example, replacing a single inflatable can cost anywhere from $3,000 to $5,000, so having protection against theft or damage is vital. This coverage ensures you won’t have to pay out of pocket for such costly replacements.

Additional Coverage Options

Beyond the basics, there are other types of insurance that can further safeguard your business.

- Commercial Auto Insurance: If you’re using vehicles to transport your equipment, this coverage is a legal requirement. It protects your business vehicles during transit.

- Workers’ Compensation: Once you hire employees or setup crews, this becomes mandatory in most states. It covers medical expenses and lost wages for job-related injuries, with costs averaging around $40 per month.

- Professional Liability (Errors & Omissions): This protects you against claims of negligence, like improper safety instructions or faulty setups. Expect to pay about $59 per month for this coverage.

- Umbrella or Excess Liability: If your primary policy limits aren’t enough, these policies provide extra coverage – sometimes up to $10 million. They’re especially useful when working with schools or corporate clients that require higher coverage amounts, such as $1 to $2 million.

- Business Owner’s Policy (BOP): This bundles general liability and property insurance into one package, typically costing about $104 per month. It’s often more economical than buying separate policies.

Some insurers also offer specialized add-ons for risks like communicable diseases, assault and battery, or allegations of sexual abuse and molestation.

"Shop around for a good broker you trust who works with a lot of businesses and markets so they can find the best price for you." – Luna Tolunay, CSEP, Fun Planners

These additional coverages provide extra peace of mind and help you manage the unique risks of running an inflatable rental business.

How Bouncy Rentals Ensures Safety and Coverage

Fully Insured Equipment and Operations

At Bouncy Rentals USA, every piece of equipment comes with full insurance coverage, offering peace of mind for all involved. Whether you’re renting a bounce house, obstacle course, or water slide, this coverage spans the entire rental period – from delivery and setup to takedown – helping to reduce personal liability risks. This is particularly important given the rise in reported injuries related to inflatable equipment. To complement this insurance, the team takes extra steps to ensure safety through detailed inspections and professional handling.

Safety Inspections and Professional Setup

Insurance is just one part of the safety equation. Bouncy Rentals USA takes proactive measures to ensure every inflatable meets local safety laws and standards. Before any rental, trained staff perform thorough inspections, checking critical components like anchor points, seams, blowers, and safety netting. Each unit is also sanitized between uses to maintain a clean and safe environment.

The setup process is handled with the same level of care. Proper anchoring, correct inflation, and clear safety instructions are all part of the professional installation. This includes establishing a safety perimeter for bounce houses to prevent accidents. This thorough approach is crucial, especially considering that injury rates for inflatables rose by 1,500% between the early 2000s and 2019. By combining these rigorous safety protocols with comprehensive liability coverage, Bouncy Rentals USA ensures a secure and enjoyable experience for every event.

How to Secure Proper Liability Coverage

Finding Qualified Insurance Providers

If you run an inflatable rental business, you’ve probably noticed that many generic insurance agents label it as "high risk." This often results in inflated premiums or policies with vague language that leave dangerous gaps in coverage. That’s why working with an industry specialist is essential. These professionals understand the unique risks, like wind-related incidents or equipment malfunctions, and can design policies that specifically address your needs.

"Simply put, you want to work with a specialist. They will get you the most specific wording in your contract to make sure your business is not at risk." – The Outdoor Play Store

When evaluating insurance providers, consider factors like your total number of units, annual revenue, and staffing requirements. These details will help determine whether you need additional coverage types, such as Workers’ Compensation or Commercial Auto insurance. Look for providers that offer 24/7 support and same-day insurance certificates for added convenience. To get the best deal, request quotes from at least three providers. Basic general liability insurance typically costs between $300 and $1,500 annually, while specialized policies start around $1,800 to $2,500 per year.

Once you’ve chosen a specialist provider, double-check that your coverage meets all venue requirements before moving forward.

Verifying Insurance Certificates and Coverage Limits

After securing a policy, take the time to verify that it fully satisfies the requirements set by your venues. Most venues require liability coverage ranging from $1 million to $2 million. Ask your provider for a Certificate of Insurance (COI) that includes both "Each Occurrence" and "General Aggregate" limits. Also, make sure the venue is listed as an "Additional Insured" on your policy.

Keep in mind that processing additional paperwork can take up to two weeks. Some insurance providers offer unlimited additional insured certificates at no extra charge, while others may apply fees. Be thorough when reviewing your policy for exclusions. Budget-friendly policies might cut corners by removing "Medical Payments" coverage or excluding certain equipment, like mechanical bulls. In some areas, tools like KwikComply.org – used by Los Angeles Parks and Recreation – can simplify the process of verifying insurance status.

Maintaining Coverage Over Time

Your liability coverage isn’t a "set it and forget it" kind of deal. Review your policy annually to ensure it keeps pace with your business needs, especially if you’re transitioning from small residential events to larger corporate or public gatherings. If you purchase new equipment, notify your insurer right away. Some providers, like The Hartford, automatically cover new inflatables for up to 45 days after purchase, but you’ll need to formally add them to your policy within that window.

Stay proactive by documenting staff training, equipment inspections, and repairs. These records not only help you comply with state regulations but also strengthen your case if you ever need to file a claim. Plus, maintaining a clean claims history can prevent your premiums from skyrocketing. To streamline the process, consider using rental management software to keep your policies updated and ensure you meet venue requirements seamlessly.

Conclusion

Liability coverage forms the backbone of safe and successful inflatable events. When a rental company has proper insurance, it’s a win for everyone: the company avoids financial disaster, event organizers steer clear of personal liability, and participants have a path to resolution if injuries occur. This type of protection isn’t just a formality – it’s central to how we operate at Bouncy Rentals USA.

"Bounce house insurance is more than a business expense – it’s an investment in your company’s future. Comprehensive coverage ensures that a single incident won’t destroy what you’ve built." – Got Inflatables

At Bouncy Rentals USA, we go beyond just offering insured equipment. Our commitment includes professional setup, regular inspections, and trained staff to monitor every event. This attention to detail, paired with comprehensive liability coverage, ensures that organizers, guests, and our reputation are all protected. Renting with us means you’re choosing safety and accountability at the highest level.

From backyard birthday parties to large school carnivals, partnering with an insured rental company safeguards your finances and opens doors to premium venues like public parks that require proof of coverage.

FAQs

What types of insurance are essential for inflatable rental businesses?

Inflatable rental businesses need to have the right insurance to handle risks and keep everyone safe. General liability insurance is a must – it covers accidents or injuries that could happen during an event. On top of that, product liability insurance protects you from claims involving defective or malfunctioning equipment.

You’ll also want workers’ compensation insurance if you have employees, as it covers workplace injuries. And don’t forget property insurance to safeguard your equipment against damage or theft. Having these policies in place not only shields your business from potential setbacks but also reassures your customers, creating a safer and more enjoyable experience for everyone.

How does weather affect the safety of inflatable rentals?

When it comes to inflatable rentals, weather can be a game-changer – especially strong winds. High winds can lift inflatables right off the ground, creating potentially dangerous situations that could result in injuries. Rain is another concern, as it can make surfaces slippery and increase the risk of accidents.

To keep everyone safe, always anchor inflatables securely and stick to the manufacturer’s safety recommendations. If bad weather is on the horizon, it’s smarter to either reschedule the event or move it indoors to avoid unnecessary risks.

How can I ensure my liability coverage meets the venue’s requirements for inflatable rentals?

When ensuring your liability coverage aligns with the venue’s requirements, begin by requesting their specific liability limits and any conditions for naming additional insured parties. Obtain a Certificate of Insurance from your provider that reflects those limits and lists the venue (or its representatives) as an additional insured. Carefully review the coverage details, including any required endorsements, against the venue’s checklist. To avoid any surprises, confirm everything with the venue through their verification process well in advance of your event date.