Running an inflatable rental business comes with risks, especially since over 18,000 injuries were linked to inflatable amusements in 2012, with nearly 90% involving children under 14. To protect your business and customers, focus on these four key strategies:

- Safety Protocols: Prevent accidents with proper setup, weather monitoring, and equipment inspections.

- Employee Training: Train staff to handle setup, supervision, and emergencies effectively.

- Insurance Coverage: Cover financial risks with general liability, accident, and property insurance.

- Liability Waivers: Use clear, legally binding waivers to reduce legal exposure.

Each approach has strengths and costs, but combining them creates a solid defense against potential risks. This article explains how to implement these strategies effectively, ensuring safety and financial protection for your business.

1. Safety Protocols

Safety protocols are essential for managing risks in inflatable rentals. They help prevent accidents by ensuring secure setups and keeping a close eye on weather conditions. These measures also tie into broader risk management efforts, including employee training and insurance coverage, which are discussed later.

Effectiveness

Proper safety protocols significantly lower the risk of injuries. For example, anchoring inflatables correctly helps prevent tipping or being lifted by strong winds. Monitoring the weather and using weather-resistant bounce houses is equally important – deflate inflatables immediately if wind speeds exceed the manufacturer’s limits or during rain or lightning. Wet surfaces and high winds can make inflatables unsafe.

Active supervision is another key factor. Grouping participants by size and age reduces the chances of collisions and promotes safer play. Trisha Sirju, Vice President and Senior Risk Consultant at Marsh Advisory, emphasizes:

Most injuries can be attributed to incorrect set-up, improper use, or unsupervised play.

Routine equipment inspections are also critical. Identifying issues like rips, weakened seams, or blower malfunctions early can prevent equipment failure.

Implementation Cost

Investing in safety protocols upfront can save money in the long run. For instance, commercial-grade inflatables may cost more initially but can last over eight years, whereas cheaper alternatives often fail after just 2.5 years. Professional training programs, such as SIOTO certification, teach staff essential skills like proper anchoring, capacity management, and emergency response.

Basic equipment requirements include outdoor-rated extension cords (no longer than 75 feet), ground fault-protected power supplies, impact-absorbing mats for entry and exit points, and wind gauges for real-time weather tracking. While these items add to operating costs, they are far less expensive than dealing with the aftermath of an accident. Standardized checklists and proper equipment also make it easier to enforce safety measures on-site.

Ease of Enforcement

Some protocols are simple to monitor visually, while others require more active oversight. For example, staff can easily check capacity limits and age-grouping compliance by observation. Setup procedures, such as anchoring and electrical safety, can be efficiently enforced using standardized checklists.

Weather monitoring demands more attention. It involves not just using wind gauges but also assigning someone to regularly assess conditions throughout the event. Similarly, ensuring participants follow rules – like removing shoes and jewelry or avoiding flips – requires constant supervision and clear signage on-site.

Liability Reduction Impact

Enforcing thorough safety protocols helps reduce liability and strengthens overall risk management. Keeping detailed logs of inspections, maintenance schedules, and staff training demonstrates to insurers that risks are being actively managed. This can result in premium discounts ranging from 25% to 40%. High-profile clients, such as schools and municipalities, often require proof of these measures along with liability coverage of $1 million to $2 million.

Gary Simon of Jungle Jumps highlights the importance of these practices:

By understanding the risks and taking the appropriate steps to reduce them, you can help protect your business and customers from potential harm.

When accidents are avoided through proper protocols, you not only save on immediate costs like medical expenses but also protect your reputation and maintain favorable insurance rates.

2. Employee Training Programs

Employee training plays a critical role in ensuring that safety procedures are consistently followed. It not only reinforces proper equipment setup and monitoring but also aligns team operations with broader risk management goals. SIOTO training programs focus on essential skills such as correct anchoring techniques, assessing weather conditions, enforcing capacity limits, and responding to emergencies. The good news? Most professional training courses can be completed in just 1 to 2 hours.

Effectiveness

Training programs address many of the common causes behind inflatable-related accidents. Staff learn to evaluate ground stability, distribute weight to prevent tipping, and monitor wind speeds to determine when deflation is necessary. They’re also trained to handle equipment malfunctions and sudden weather changes with confidence. As SIOTO points out:

Safety is the cornerstone of a reputable inflatable rental business.

Beyond improving safety, certification can give your business a competitive edge. Schools, churches, and corporate clients often require proof of training before signing contracts. Displaying certification seals on your website and marketing materials can build trust and showcase your commitment to high safety standards. This solid training foundation helps ensure consistent application of safety protocols at every event.

Implementation Cost

The Advanced Inflatable Safety Operations Certification (AISOC) costs $299 per operator. While this may seem like a significant upfront expense, it can pay off in the long run. Many insurance providers recognize the value of certifications and may offer reduced premiums to businesses with trained staff. Scheduling training during the off-season can also help you prepare your team without disrupting peak operations.

Ease of Enforcement

Standardized tools like checklists and certification programs make it easier to enforce safety protocols. For instance, daily inspection routines before and after rentals can help identify wear and tear early. Certifications, which should be renewed every 1 to 2 years, ensure that your team stays up-to-date with the latest safety standards. Plus, online verification tools allow clients and insurers to quickly confirm your staff’s credentials.

Liability Reduction Impact

Documented training provides a clear record for insurance compliance and legal defense, which is crucial in the event of an incident. This documentation complements safety logs and inspection records, creating a comprehensive approach to risk management. Proper training not only helps prevent accidents but also reduces the chances of costly lawsuits, medical expenses, and damage to your reputation. For context, wind-related incidents have caused 479 injuries and 28 fatalities since 2000. As SIOTO highlights:

Certification provides peace of mind to those renting inflatables for children and guests.

When combined with other safety measures, employee training forms a critical part of an effective risk management strategy.

3. Insurance Coverage Types

When preventive measures like safety protocols and employee training fall short, insurance coverage steps in to protect your business financially. It’s a critical component of any risk management strategy, especially in industries where accidents can happen despite the best precautions.

General liability insurance is the cornerstone of this protection, covering third-party bodily injury and property damage claims. Standard coverage limits are typically $1 million per occurrence and $2 million aggregate. Basic annual premiums range from $300 to $1,500. For high-risk or high-value venues, such as hotels or corporate events, liability limits may need to rise to $3 million or even $5 million. Mark Fitzpatrick, a Licensed Property and Casualty Insurance Producer, emphasizes:

General liability insurance is the most critical coverage for bounce house businesses due to high injury risk from children using inflatables.

Participant accident insurance provides an extra layer of protection by covering minor medical expenses without requiring proof of negligence. With premiums starting around $350 per year, this coverage can address small incidents – like a child breaking an arm – before they escalate into costly lawsuits. Alex Cossio, Area Vice President at Replacement Services, notes:

Participant accident insurance acts as a ‘sacrificial lamb’ to prevent claims against the general liability policy by covering out-of-pocket costs and reducing the likelihood of lawsuits.

This type of policy is especially useful for handling minor accidents, helping to avoid larger legal battles. Beyond these foundational policies, there are several other specialized coverages to consider.

Professional liability insurance protects against negligence claims, such as improper setup, failure to anchor equipment securely, or inadequate safety instructions. Inland marine insurance safeguards your equipment while it’s being transported or stored, with coverage amounts typically ranging from $25,000 to $75,000 depending on your inventory. Property insurance, which generally costs 1% to 2% of your inventory’s total value annually, covers damages to your business property. Additionally, workers’ compensation insurance is vital for covering injuries sustained by employees on the job.

If you’re hosting events at schools, parks, or other public venues, you’ll often need a Certificate of Insurance (COI). These are typically required 14 to 30 days before the event. Adding a venue as an "Additional Insured" to your policy usually costs between $25 and $50 per certificate. To ensure comprehensive protection, it’s best to opt for occurrence-based policies, which cover incidents that happen during the policy period, even if claims are filed later.

You can also save on premiums by bundling multiple policies with one provider or maintaining detailed safety training records, which may reduce premiums by up to 20%. These strategies not only help manage costs but also ensure your business is well-prepared for unforeseen challenges.

4. Liability Waivers and Contracts

Insurance offers financial security, but liability waivers and contracts serve as your first line of defense. A well-drafted waiver not only reduces legal risks but also reflects professionalism. Here’s how these documents strengthen your business’s liability protection.

Effectiveness

Liability waivers work best when written in plain, straightforward language. This approach ensures customers fully grasp the rights they’re giving up and the responsibilities they’re taking on. Key elements of an effective waiver include:

- Clearly defined rental terms

- Waivers of rights explained in simple terms

- Specific payment terms, including late fees

- Penalties for breaches of contract

To make the document legally binding, both parties must sign and date it.

Adding an indemnification clause can further protect your business. This clause requires customers to defend and hold your company harmless if claims arise from their equipment use. Including an arbitration clause is another smart move, as it helps avoid lengthy court battles. Additionally, tailor your contract to address event-specific conditions that align with your safety measures.

Implementation Cost

The cost of liability waivers is minimal compared to the protection they offer. Attorney-reviewed templates are a one-time investment that can save you significant legal headaches. These waivers work hand-in-hand with insurance, which for smaller businesses typically costs $500 to $1,000 annually. As the JumpOrange Marketing Team puts it:

Advertising that your business is insured communicates professionalism and responsibility… insurance is not just protection – it’s also a sales tool.

Liability Reduction Impact

When executed properly, waivers play a key role in reducing legal risks. They set clear guidelines for equipment use, outline customer responsibilities, and address issues like weather-related cancellations. Providing customers with copies of the waiver and using clear language fosters trust and ensures everyone is on the same page.

Combined with standard $1M–$2M liability insurance coverage, waivers create a strong safety net against claims. Alongside safety protocols, employee training, and insurance, these contracts help build a comprehensive risk management strategy.

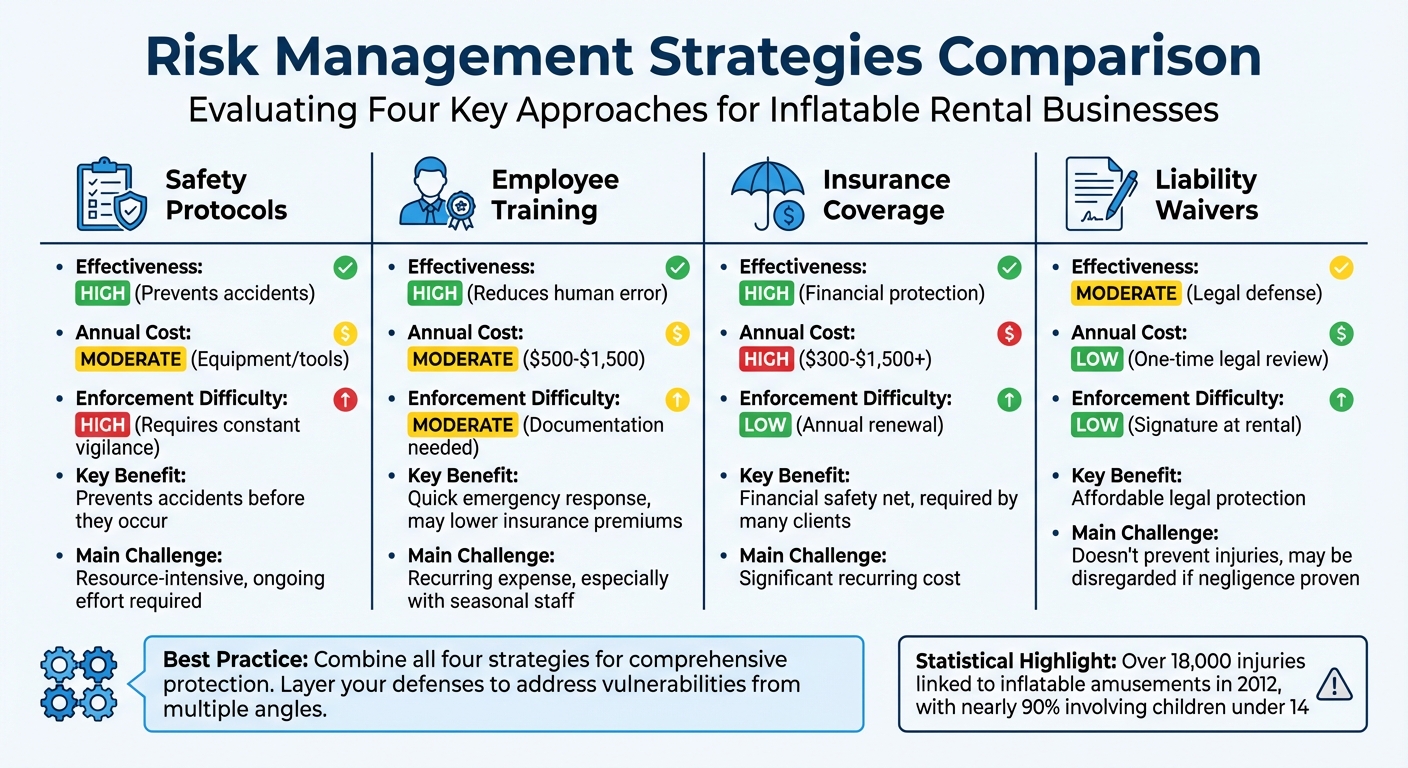

Advantages and Disadvantages of Each Strategy

Risk Management Strategies for Inflatable Rentals: Comparison of Effectiveness, Cost, and Implementation

Each risk management strategy comes with its own set of benefits and challenges. By comparing these approaches side by side, we can better understand the trade-offs involved.

Safety Protocols are excellent at preventing accidents before they happen. Regular inspections can catch wear and tear early, while proper anchoring and consistent weather monitoring help avoid serious equipment failures. These measures not only enhance safety but also build trust among customers. However, they require ongoing effort and constant vigilance, which can be resource-intensive.

Employee Training focuses on minimizing human error by ensuring staff are well-prepared for proper setup and emergencies. Trained employees can respond quickly and effectively in critical situations, and certifications like SIOTO may even lower insurance premiums. On the downside, training programs – especially refresher courses – can become a recurring expense, particularly for businesses that rely on seasonal staff.

Insurance Coverage acts as a financial safety net, covering costs that physical precautions alone might not prevent. For example, in one incident, a deflation event led to three injuries and $95,500 in medical and legal expenses – all of which were covered by general liability insurance. Additionally, many schools and municipalities require compliance with local safety laws and proof of insurance before signing contracts. While insurance premiums can be a significant recurring cost, the financial risks of operating without coverage are far greater.

The table below provides a quick comparison of these strategies in terms of effectiveness, cost, and enforcement challenges:

| Strategy | Effectiveness | Annual Cost | Enforcement Difficulty |

|---|---|---|---|

| Safety Protocols | High (prevents accidents) | Moderate (equipment/tools) | High (requires constant vigilance) |

| Employee Training | High (reduces human error) | Moderate ($500–$1,500) | Moderate (documentation needed) |

| Insurance Coverage | High (financial protection) | High ($300–$1,500+) | Low (annual renewal) |

| Liability Waivers | Moderate (legal defense) | Low (one-time legal review) | Low (signature at rental) |

Liability Waivers are among the most affordable strategies. A one-time legal review can create reusable templates that help shift certain risks to customers. They also serve as valuable documentation in legal disputes. However, waivers don’t prevent injuries, and courts may disregard them if negligence – like poor equipment maintenance or improper setup – is proven. This makes liability waivers a useful supplement to other strategies but not a standalone solution for risk management.

Conclusion

Combining multiple risk management strategies is the best way to protect your business effectively. A layered defense system that includes safety protocols, employee training, insurance coverage, and liability waivers ensures that different vulnerabilities are addressed from all angles.

Your investment in risk management should match the size and scope of your business. For small operations, such as those focused on backyard parties, starting with general liability insurance (which typically costs between $300 and $1,500 annually) and standardized rental agreements is a solid foundation. Medium-sized businesses with multiple units and employees should consider adding property insurance to safeguard inventory and workers’ compensation to protect their team. For larger businesses, especially those serving schools or municipalities, liability limits of $2 million or more and umbrella policies become essential to handle more complex risks. This scalable approach ensures that your risk management evolves alongside your business.

Some safety practices, however, apply universally – no matter the size of your operation. Daily equipment inspections, keeping a close eye on weather conditions, and requiring signed liability waivers from every customer are non-negotiable. As Gary Simon from Jungle Jumps explains:

Liability is the legal responsibility for any losses or damage caused to another person or business as a result of your work.

While insurance is a critical safety net, it cannot replace the need for active and consistent safety measures.

A great example of this balanced approach is Bouncy Rentals USA. They ensure their equipment is sanitized after every rental, fully insured, and delivered by trained staff. This kind of integration – combining safety protocols, training, insurance, and legal protections – demonstrates how these principles work together to create a safe and reliable operation.

Finally, thorough documentation ties all of these strategies together. Detailed records are your strongest legal defense. Maintain logs of inspections, repairs, training sessions, and weather conditions. These documents provide proof that you’ve taken every reasonable precaution to uphold your duty of care.

FAQs

What wind speed is too dangerous for inflatables?

Inflatables can quickly become hazardous when wind speeds exceed 15-20 mph. Strong winds may cause them to lift off the ground or become unstable, posing serious safety risks. To prevent accidents, it’s crucial to monitor wind conditions closely and ensure inflatables are securely anchored before use.

What paperwork should I keep to prove I followed safety rules?

To demonstrate compliance with safety rules for inflatable rentals, it’s important to keep thorough documentation. This includes rental agreements that outline safety protocols, liability waivers, and any safety instructions provided by the rental company. If you employ operators, ensure you have records of their training and instructions.

For events, maintain documentation like permits, safety checklists, and supervision policies. These records not only help you stay organized but also serve as proof that you’ve followed safety standards.

Do liability waivers still help if someone gets hurt?

Yes, liability waivers can help shield businesses or individuals from certain injury claims if they are well-written and properly enforced. However, they do not protect against claims involving gross negligence or intentional wrongdoing. To ensure their effectiveness, waivers must be clearly written, easy to understand, and adhere to local legal requirements.